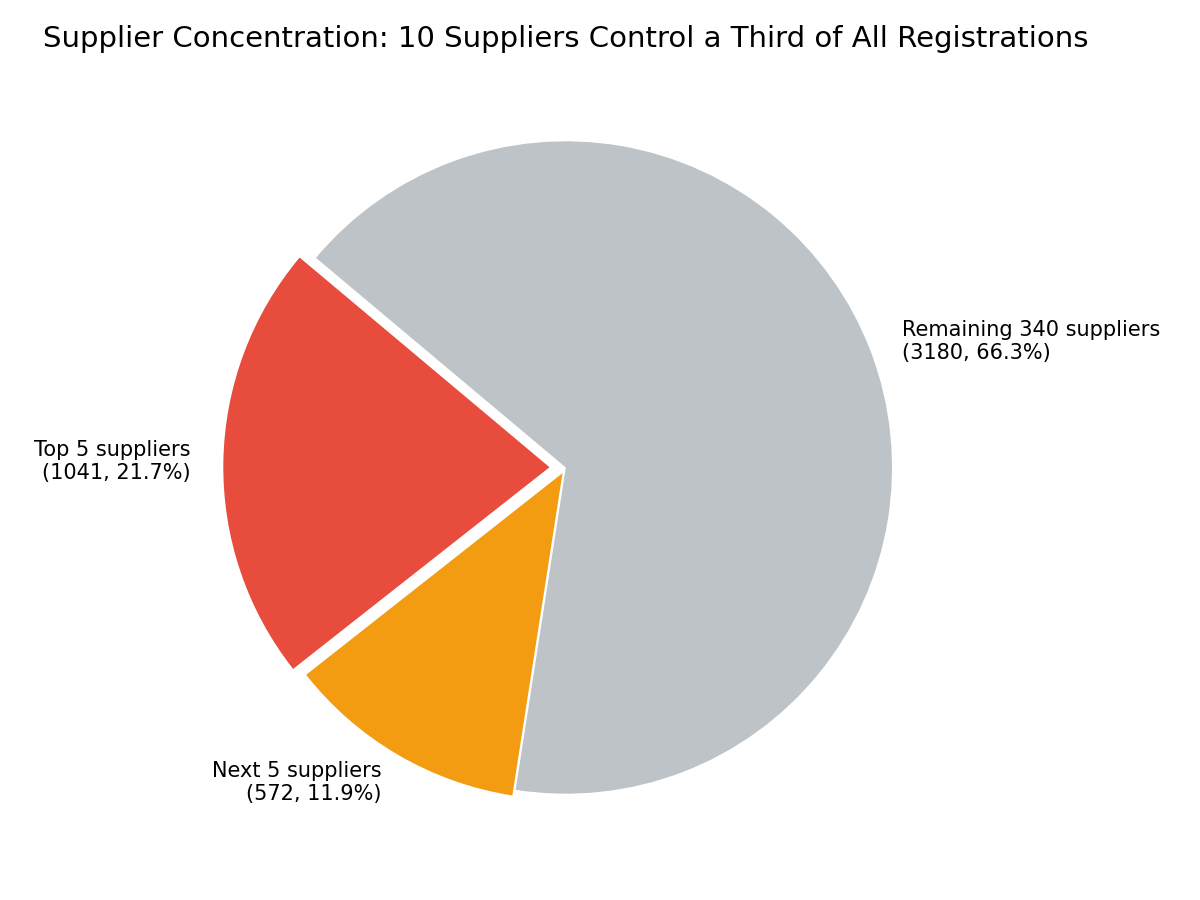

UAE EDE: 10 Suppliers Control a Third of All Medical Device Registrations

UAE EDE data shows 10 suppliers control 33.7% of 4,793 medical device registrations. Cigalah, Pharmatrade lead. US tops country of origin at 16%. Dubai holds 63.5% of registrations.

Executive Summary

The United Arab Emirates has completed a landmark regulatory restructuring: as of January 2026, the Emirates Drug Establishment (EDE) is the sole federal authority for medical device classification, market authorization, import permits, and post-market vigilance — absorbing 44 core regulatory services previously managed by the Ministry of Health and Prevention (MOHAP). Registration validity remains five years, with renewals now processed through the EDE digital portal.

Our analysis of the complete EDE medical device register (extracted 5 June 2026, 4,793 active device rows) reveals a highly concentrated supplier landscape with important implications for market-entry strategy:

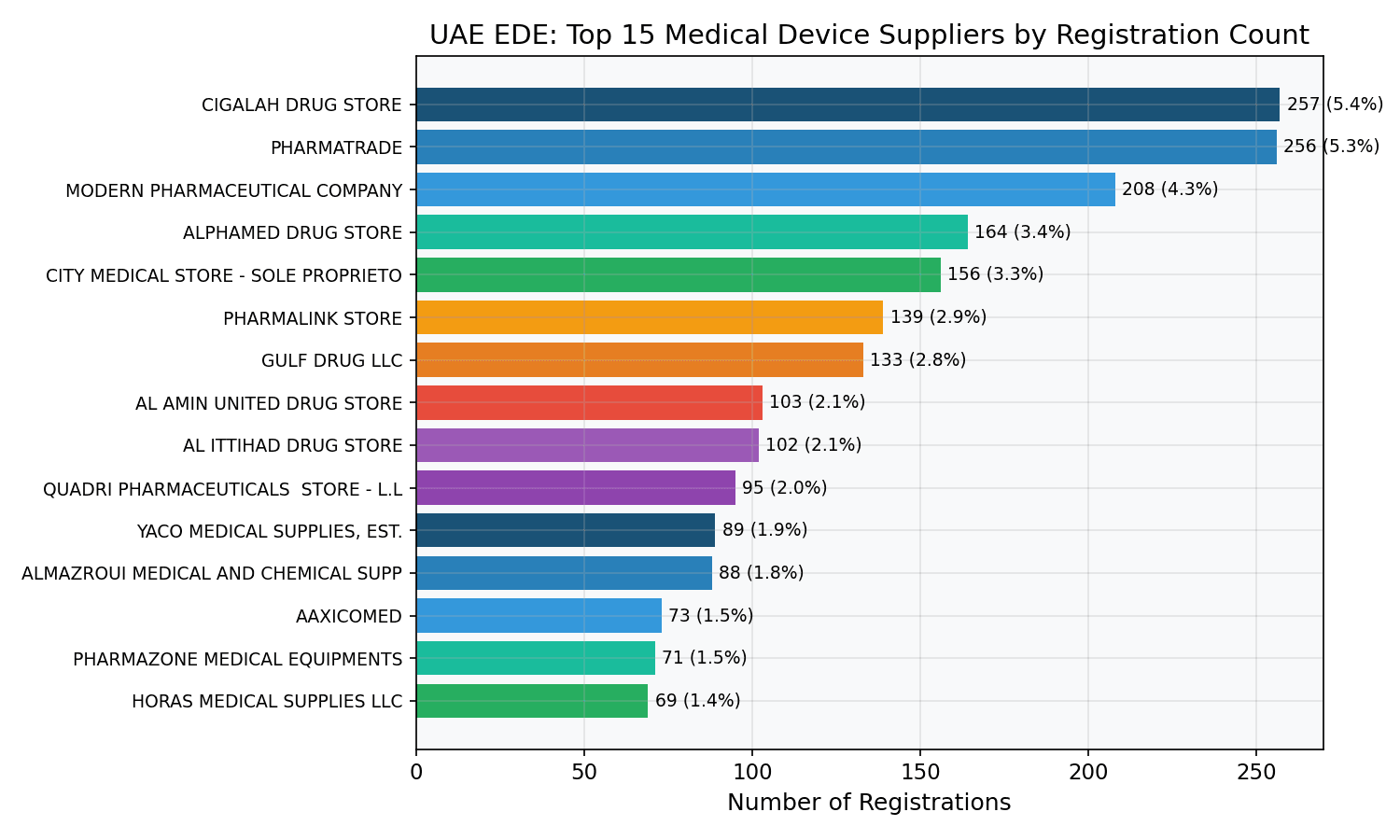

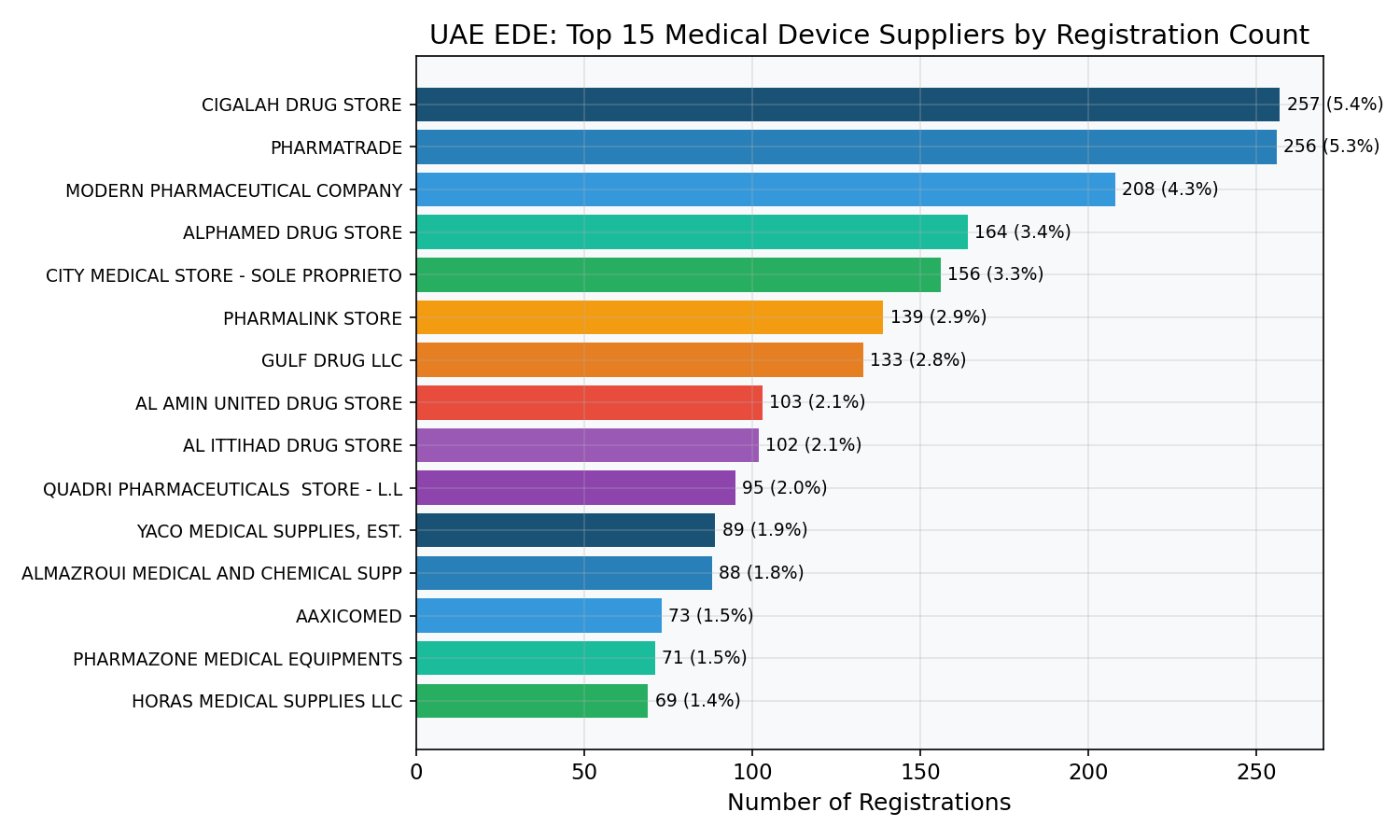

- 10 suppliers control 33.7% of all active medical device registrations, with Cigalah Drug Store (257), Pharmatrade (256), and Modern Pharmaceutical Company (208) forming a clear top tier

- 350 unique suppliers serve 913 manufacturers across 56 countries of origin — a ratio of 2.6 manufacturers per supplier that signals heavy channel consolidation

- The United States is the top country of origin at 16.0% (765 registrations), followed by China and Italy tied at 10.4% each (497 registrations)

- Dubai-based suppliers hold 63.5% of registrations (3,044), with Abu Dhabi at 25.9% — reflecting the emirate's dominance as the UAE's medical device distribution hub

- Registration volumes peaked in 2021 at 810 new registrations, a 62% increase over 2019 levels, driven by COVID-era demand and regulatory modernization

Regulatory Context: MOHAP to EDE Transition

On 2 January 2025, Federal Decree-Law No. 38 of 2024 came into force, establishing the EDE as the UAE's federal authority for regulating medical products, including medical devices and IVDs. By December 2025, EDE had formally assumed 44 specific regulatory services from MOHAP, including medical device classification, market authorization, import permits, manufacturer licensing, and post-market vigilance (RegDesk, January 2026).

Key changes for device manufacturers:

- All submissions now flow through the EDE digital portal, requiring UAE PASS login and registered organization accounts

- Registrations remain valid for five years from the date of last approval, with renewals processed through EDE (OMC Medical, 2026)

- A Local Authorized Representative (LAR) is mandatory for foreign manufacturers without a direct UAE presence — the LAR manages regulatory submissions and compliance on the manufacturer's behalf

- Government fees for first-time market entry total approximately 16,100 AED (~USD 4,400), with total project costs typically ranging from $15,000 to $50,000+ including LAR fees, documentation, and consulting (MedDeviceGuide, 2026)

- In February 2026, the EDE activated a landmark anti-monopoly mechanism under Federal Decree-Law No. 38 of 2024, requiring companies to appoint more than one agent for each medical product distributed in the UAE and ending the previous single-distributor monopoly model (Middle East Briefing, February 2026; MedDeviceGuide, 2026). This policy directly targets the concentration patterns documented in this analysis and may gradually reduce the dominance of top-tier suppliers.

The UAE medical devices market was valued at approximately $3.18 billion in 2025 and is projected to reach $4.71 billion by 2032, growing at a CAGR of 5.8% (Fortune Business Insights, 2026).

Data Source and Method

- Source: EDE Drug Directory public register, accessed via

services.ede.gov.ae/drugdirectory - Analysis sample: EDE Drug Directory medical-device extract dated 5 June 2026 — 4,793 active medical device rows (part of the broader 16,939-product register that also includes pharmaceuticals and other regulated products)

- Fields analyzed: Product Name, Manufacturer, Supplier Name, Supplier Address, Country of Origin, Classification, Dispensing Mode, Registration Date, Status

- Run date: 2026-06-05

- Method: All figures computed by MedDeviceGuide analysis of the EDE public-register extract. Registration counts reflect unique product-pack-size combinations, not distinct device models. "Country of Origin" reflects the manufacturer's declared country, which may differ from the brand's corporate headquarters.

Supplier Concentration: A Handful of Gatekeepers

The 4,793 active medical device registrations are distributed across 350 unique suppliers — but this apparent diversity masks steep concentration:

| Tier | Suppliers | Registrations | Share |

|---|---|---|---|

| Top 5 | Cigalah, Pharmatrade, Modern Pharma, Alphamed, City Medical | 1,041 | 21.7% |

| Top 10 | + Pharmalink, Gulf Drug, Al Amin, Al Ittihad | 1,613 | 33.7% |

| Top 20 | + 10 more | 2,305 | 48.1% |

| Remaining 330 | Long-tail suppliers | 2,488 | 51.9% |

Cigalah Drug Store (257 registrations, 5.4%) and Pharmatrade (256, 5.3%) are nearly tied at the top, followed by Modern Pharmaceutical Company (208, 4.3%). These three alone hold 15% of all registrations.

For manufacturers entering the UAE market, this means the LAR/supplier choice is both critical and constrained. The top 10 suppliers are well-known distribution houses with established EDE relationships, cold-chain logistics, and pharmacy/hospital networks across all seven emirates. New entrants often default to these names — reinforcing concentration further.

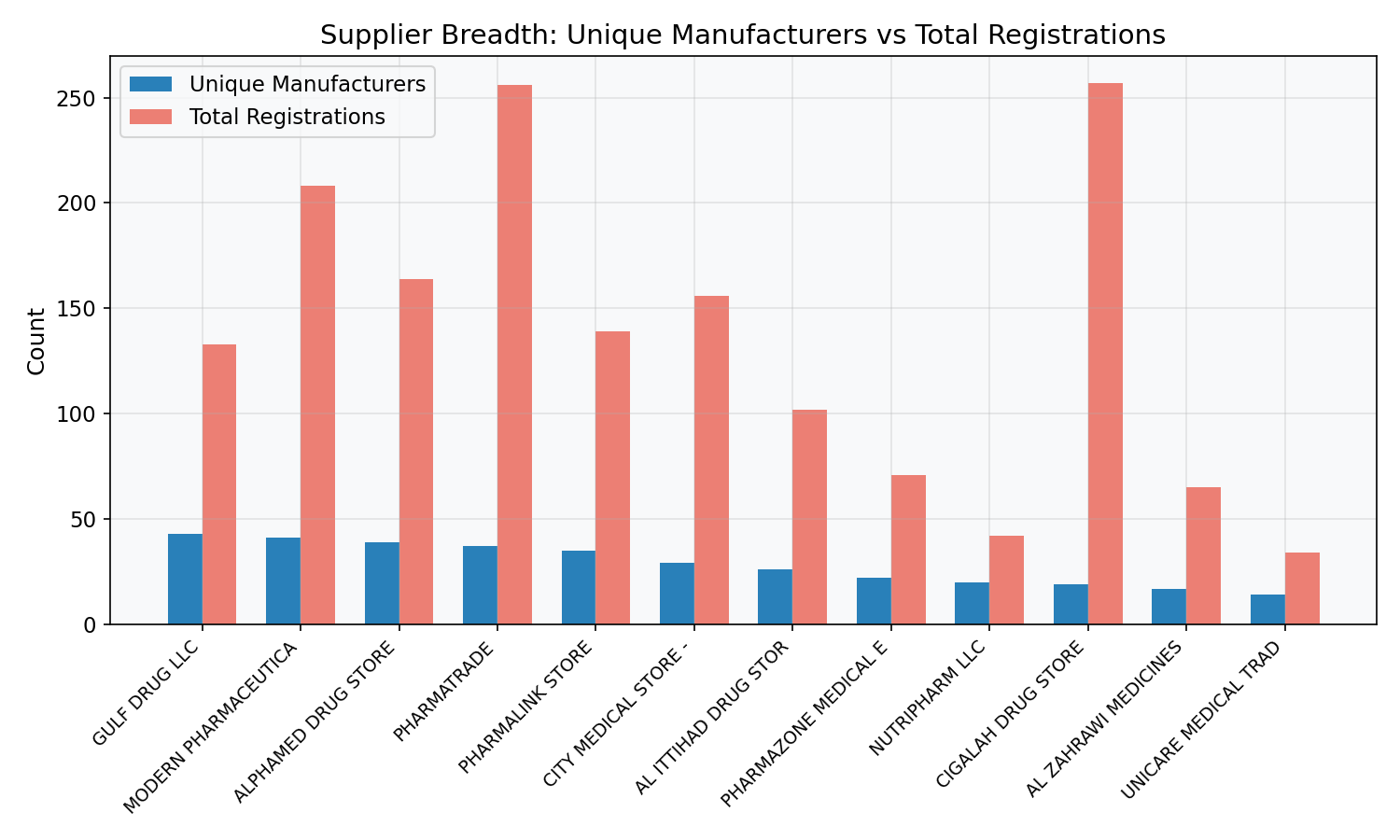

Supplier Breadth: Who Carries the Most Manufacturers?

Not all large suppliers are equally diversified. Gulf Drug LLC carries products from 43 unique manufacturers across 13 countries — the widest manufacturer network of any supplier despite ranking 7th in total registrations (133). By contrast, Cigalah Drug Store has only 19 manufacturers despite holding the most registrations (257), indicating it carries many product variants from a concentrated set of manufacturing partners.

| Supplier | Registrations | Unique Manufacturers | Countries Sourced |

|---|---|---|---|

| Gulf Drug LLC | 133 | 43 | 13 |

| Modern Pharmaceutical Company | 208 | 41 | 14 |

| Alphamed Drug Store | 164 | 39 | 11 |

| Pharmatrade | 256 | 37 | 11 |

| Pharmalink Store | 139 | 35 | 17 |

| City Medical Store | 156 | 29 | 10 |

| Cigalah Drug Store | 257 | 19 | 12 |

Pharmalink Store sources from 17 countries — the widest geographic spread — suggesting it serves as a multi-regional aggregator rather than a single-origin specialist.

For manufacturers, this breadth analysis matters: a supplier with 40+ manufacturer relationships may be harder to prioritize your product within their portfolio, but they offer broader market reach. A supplier with fewer, deeper relationships may give your product more attention.

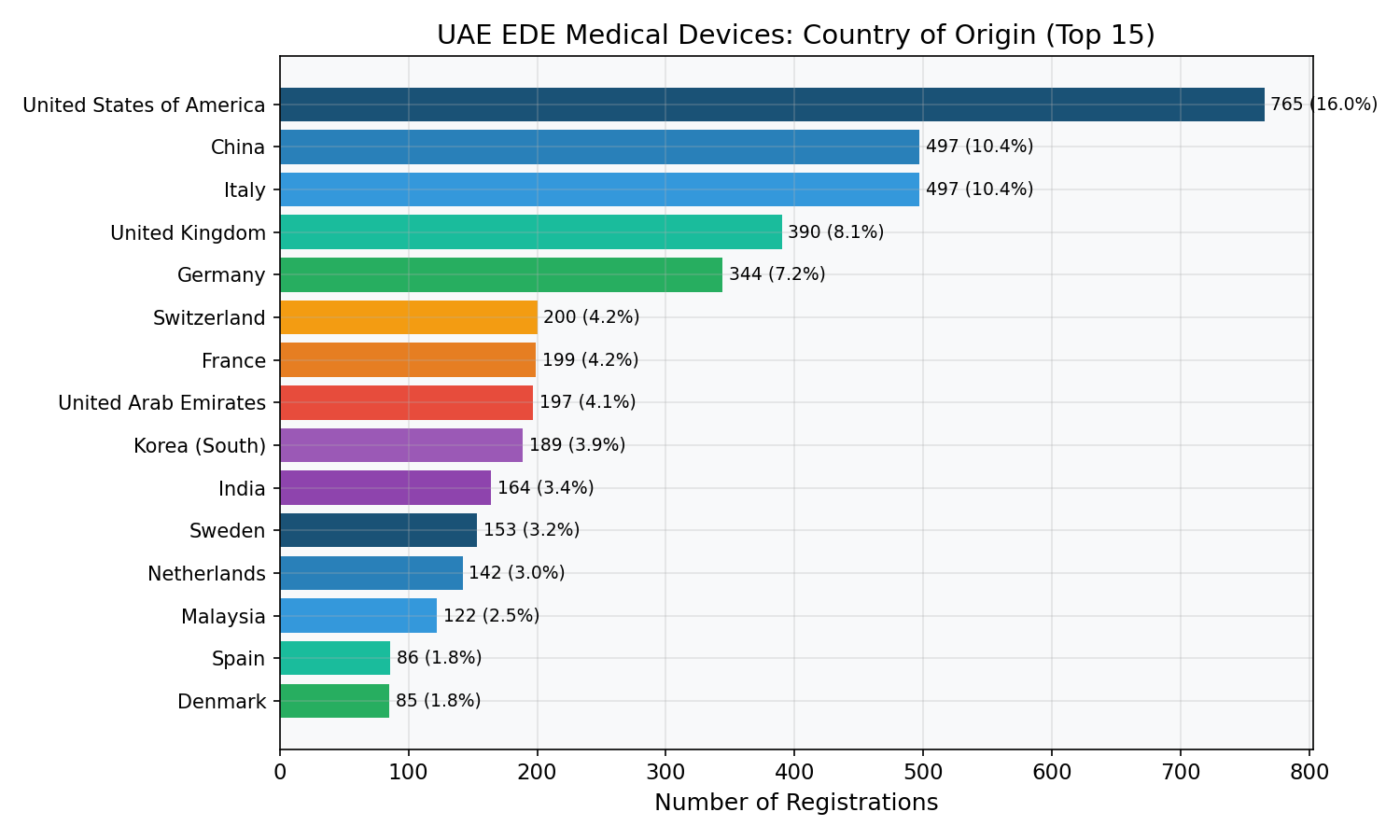

Country of Origin: US Leads, China and Italy Tie for Second

| Country | Registrations | Share | Unique Suppliers |

|---|---|---|---|

| United States | 765 | 16.0% | 80 |

| China | 497 | 10.4% | 67 |

| Italy | 497 | 10.4% | 98 |

| United Kingdom | 390 | 8.1% | 35 |

| Germany | 344 | 7.2% | 50 |

| Switzerland | 200 | 4.2% | 38 |

| France | 199 | 4.2% | 38 |

| UAE (domestic) | 197 | 4.1% | 26 |

| South Korea | 189 | 3.9% | 59 |

| India | 164 | 3.4% | 20 |

The United States dominates at 16.0% of all registrations, reflecting the strong presence of US-branded medical devices (J&J Vision Care, ArthroCare, KCI/3M, Establishment Labs, etc.) in the UAE market. However, US registrations are served by 80 suppliers — the highest supplier count of any country — indicating that US manufacturers are not locked into a single channel but are broadly distributed across the supplier landscape.

Italy's high position (10.4%, 98 suppliers) is notable: Italy has the most suppliers of any country despite ranking tied for second in registrations. This suggests Italian medical device products — likely wound care dressings, surgical instruments, and consumables — are distributed through many small-to-medium channels rather than concentrated with a few distributors.

Domestic UAE manufacturing accounts for 197 registrations (4.1%) across 26 suppliers, a modest but growing segment consistent with the UAE's push for local production under its economic diversification agenda.

South Korea (189 registrations, 59 suppliers) shows a high supplier-to-registration ratio (3.2 registrations per supplier), indicating Korean device manufacturers have yet to consolidate their UAE distribution and are often working with smaller, specialized channels.

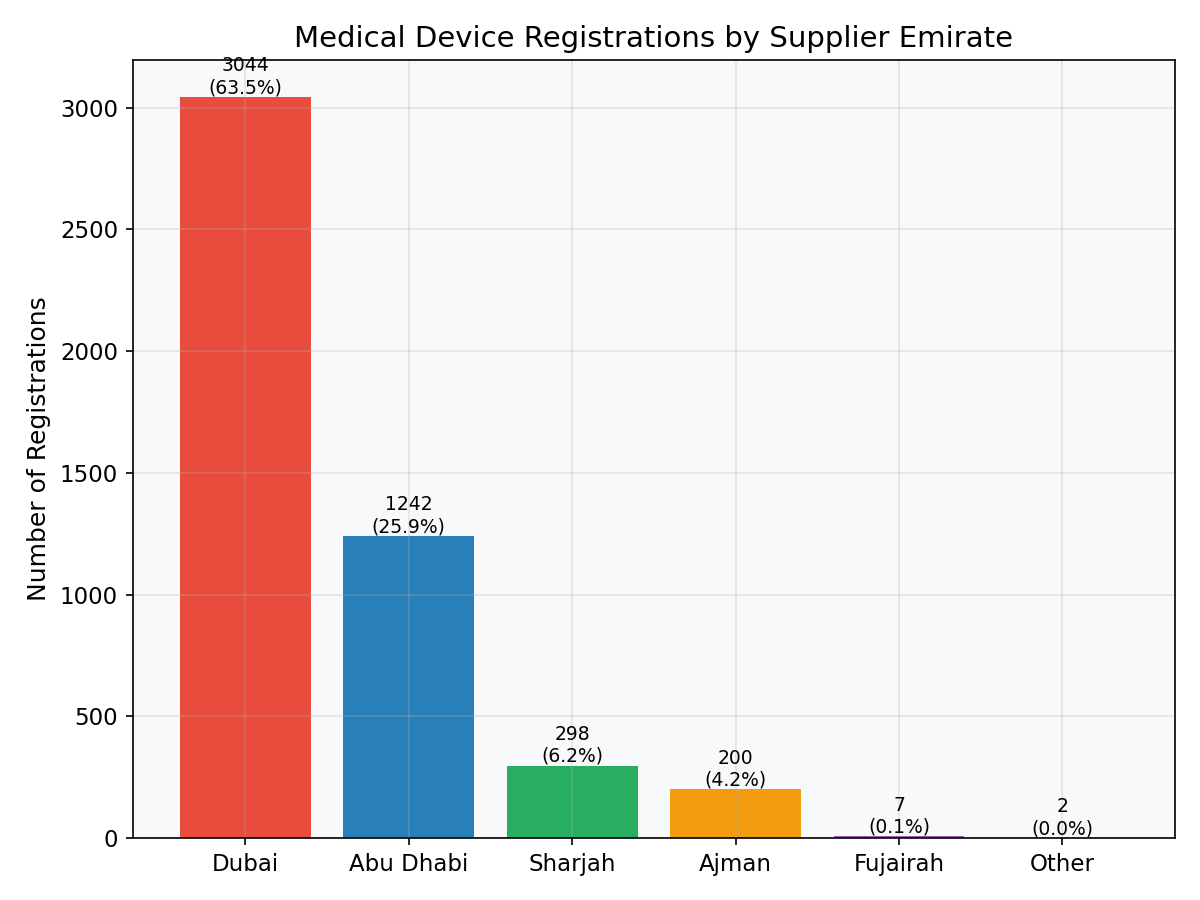

Emirate Distribution: Dubai Is the Distribution Capital

| Emirate | Registrations | Share |

|---|---|---|

| Dubai | 3,044 | 63.5% |

| Abu Dhabi | 1,242 | 25.9% |

| Sharjah | 298 | 6.2% |

| Ajman | 200 | 4.2% |

| Fujairah | 7 | 0.1% |

| Others | 2 | 0.0% |

Dubai-based suppliers hold nearly two-thirds of all medical device registrations. This reflects Dubai's role as the UAE's primary logistics and distribution hub, anchored by free zones like Dubai Healthcare City (DHCC) and Jebel Ali Free Zone (JAFZA) that offer 100% foreign ownership and streamlined licensing.

Abu Dhabi, despite being the larger healthcare spender (the emirate commands approximately 27% of UAE medical device contract manufacturing market share per Credence Research), holds 25.9% of registrations. The gap reflects the distribution-layer concentration in Dubai — many Abu Dhabi–served hospitals and clinics source products through Dubai-registered suppliers.

For manufacturers, this means most LAR/supplier relationships will be Dubai-based regardless of where the end customers are located.

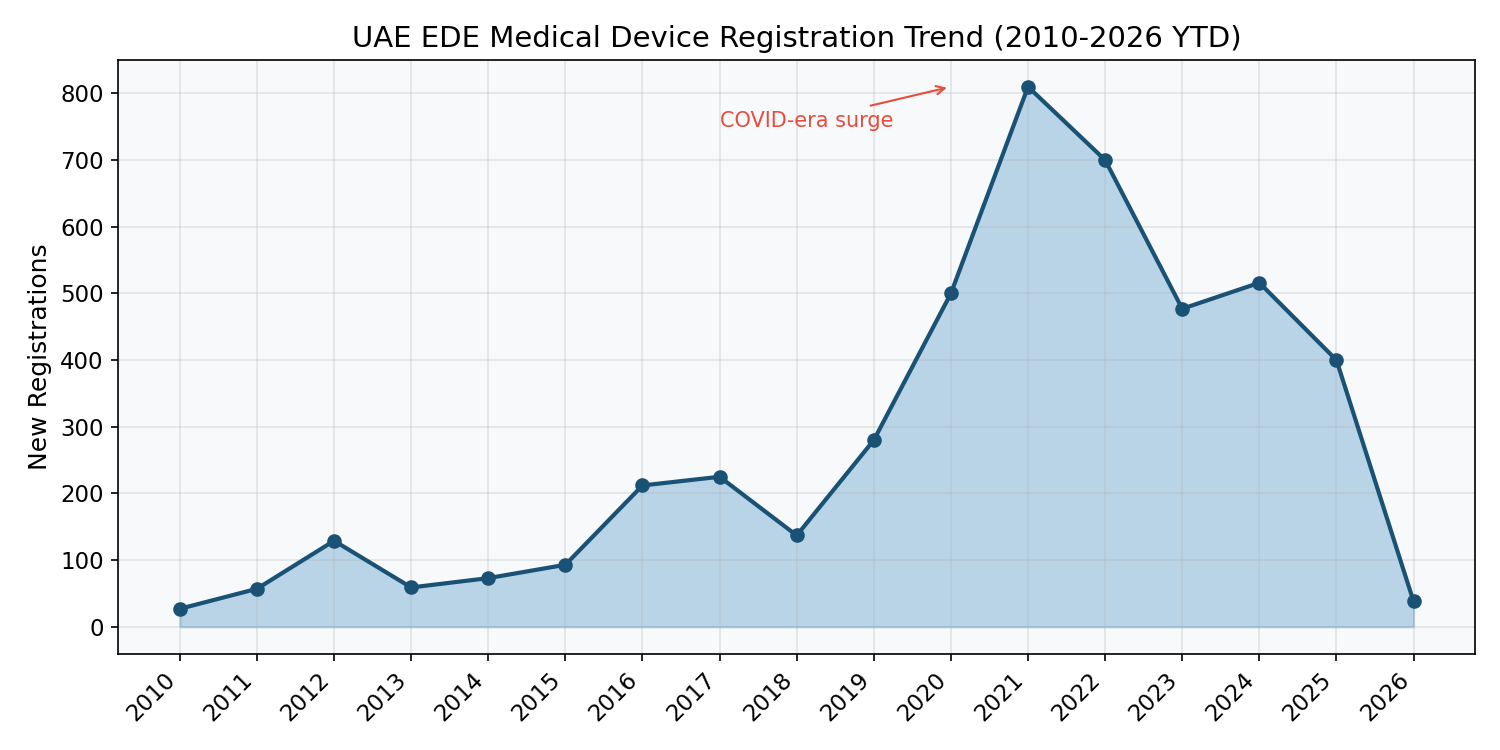

Registration Trends: COVID-Era Surge and New Normal

| Year | New Registrations |

|---|---|

| 2016 | 212 |

| 2017 | 225 |

| 2018 | 137 |

| 2019 | 280 |

| 2020 | 500 |

| 2021 | 810 |

| 2022 | 700 |

| 2023 | 477 |

| 2024 | 516 |

| 2025 | 400 |

| 2026 (Jan–May) | 38 |

The 2020–2021 period saw a massive registration surge, with 2021 recording 810 new registrations — nearly triple 2019 levels (280) and a 62% increase over the already-elevated 2020 figure (500). This was driven by COVID-19–related demand for diagnostics, PPE, respiratory devices, and monitoring equipment, combined with regulatory streamlining under MOHAP's digital portal.

The post-COVID normalization is clear: registrations settled at 477–516 annually in 2023–2024, with 2025 tracking at 400 (likely reflecting the MOHAP-to-EDE transition period disrupting normal processing). The 2026 figure of 38 registrations through May is expected to accelerate as the EDE portal matures.

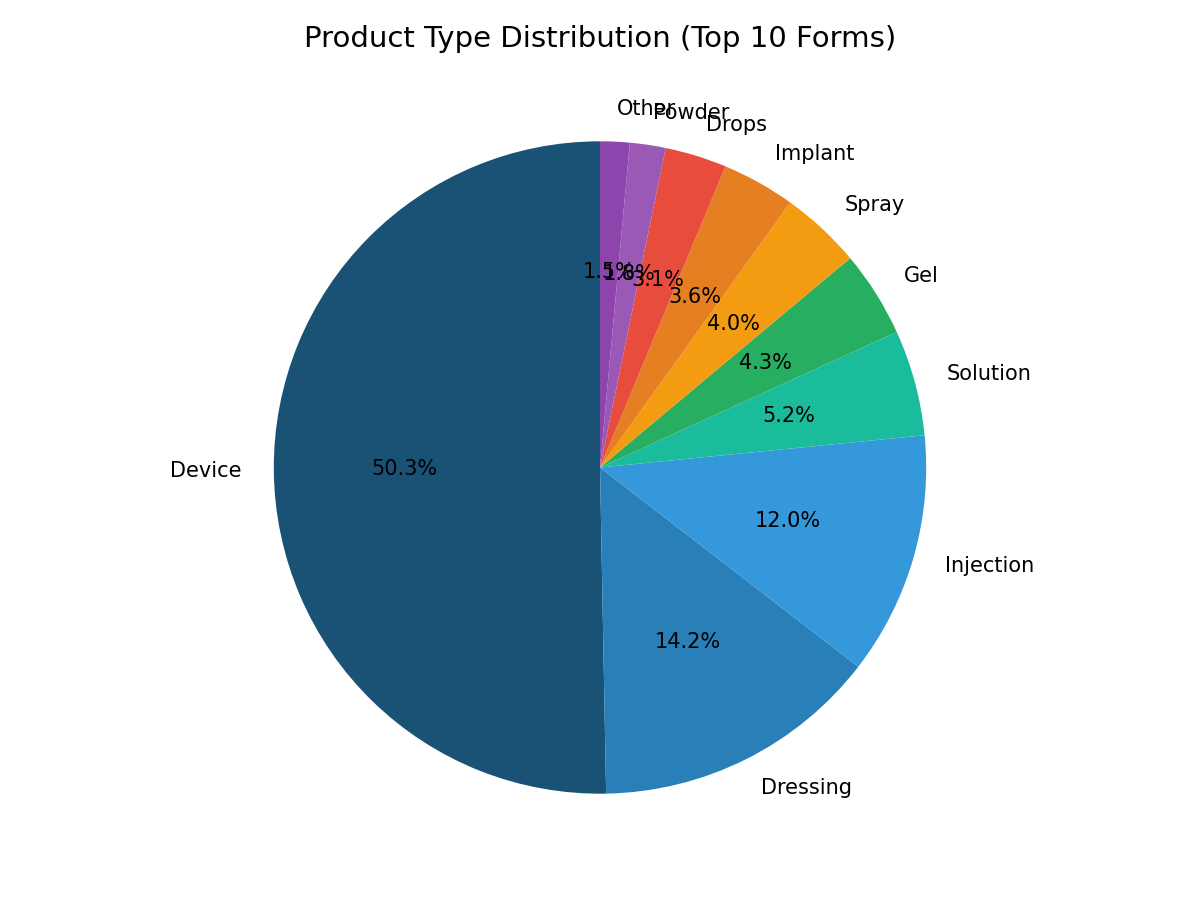

Product Types: Devices and Dressings Dominate

| Product Form | Registrations | Share |

|---|---|---|

| Device (general) | 2,274 | 47.4% |

| Dressing | 644 | 13.4% |

| Injection | 544 | 11.3% |

| Solution | 237 | 4.9% |

| Gel | 193 | 4.0% |

| Spray | 181 | 3.8% |

| Implant | 164 | 3.4% |

| Drops | 138 | 2.9% |

| IVD Test Kit | 44 | 0.9% |

The high share of dressings (13.4%) is consistent with the presence of wound-care manufacturers like Mölnlycke (52 registrations), Aroa Biosurgery (73), and Laboratoires Urgo (41) among the top manufacturers. Dressings and wound care are relatively low-risk, high-volume product categories that are well-suited to the UAE's multi-supplier distribution model.

Implants (164, 3.4%) are a higher-risk category that typically requires more rigorous EDE review. Despite their smaller registration count, implants often carry higher per-unit value and are more likely to involve direct manufacturer–hospital relationships.

Dispensing Channels

| Dispensing Mode | Registrations | Share |

|---|---|---|

| Health Care Professional's Only | 1,577 | 32.9% |

| Pharmacy Only (P) | 1,277 | 26.6% |

| Prescription Only (POM) | 1,129 | 23.6% |

| General Sale Supermarket | 348 | 7.3% |

| OTC-General Sale | 187 | 3.9% |

| Hospitals Only | 173 | 3.6% |

| OTC-Pharmacy | 68 | 1.4% |

The 32.9% "Health Care Professional's Only" segment confirms that a third of registered devices are intended for clinical/professional use — ranging from surgical instruments and implants to diagnostic equipment. The 26.6% "Pharmacy Only" and 23.6% "Prescription Only" segments together cover another half of registrations, reflecting the pharmacy-channel importance for devices like contact lenses, glucose monitors, syringes, and wound dressings.

Practical Implications for Market Entry

1. Choose Your LAR Strategically

The supplier concentration data shows that the top 10 suppliers are not interchangeable. Gulf Drug and Modern Pharma offer the widest manufacturer networks (41–43 unique manufacturers), making them suitable for manufacturers who want broad market coverage. Cigalah carries fewer manufacturers but has the most registrations — potentially indicating deeper partnerships with those manufacturers.

2. US and EU Manufacturers Face More Competition

US (16%), Italian (10.4%), UK (8.1%), and German (7.2%) manufacturers collectively account for 41.7% of registrations. Manufacturers from these regions should expect a competitive UAE market with established channel relationships. Differentiation through clinical evidence, regulatory reliance pathways (FDA clearance or CE marking accelerate UAE review), and Arabic-language documentation quality becomes critical.

3. Asian Manufacturers Are Underpenetrated but Growing

China (10.4%), South Korea (3.9%), India (3.4%), and Japan (1.1%) collectively hold 18.8% of registrations despite being among the world's largest medical device manufacturing bases. The high supplier-per-registration ratio for Korean (3.2x) and Italian (5.0x) products suggests fragmented distribution that could benefit from consolidation.

4. Factor in the EDE Transition

The MOHAP-to-EDE transfer completed in early 2026 means some historical registrations may require migration or re-submission through the EDE portal. Manufacturers should confirm their existing registrations have migrated successfully and that their LAR's EDE portal access is operational. The 2025 registration dip (400 vs. 516 in 2024) likely reflects transitional disruptions.

5. The Anti-Monopoly Rule Changes the Game

The February 2026 EDE requirement for multiple agents per product directly challenges the concentration patterns shown in this analysis. While the current register still reflects the legacy single-distributor model (Cigalah, Pharmatrade, and Modern Pharma holding dominant positions), the new rule means manufacturers must now plan multi-agent distribution strategies from the outset. Over time, this policy should dilute the top-10 concentration, but the transition period creates both complexity (managing multiple agent relationships) and opportunity (new market entrants can compete for distribution rights previously locked by incumbents).

6. Dubai Presence Is Table Stakes

With 63.5% of registrations held by Dubai-based suppliers, manufacturers should prioritize LARs with Dubai operations — even if their primary hospital customers are in Abu Dhabi. The distribution infrastructure is simply more developed in Dubai, with JAFZA and DHCC providing established frameworks for medical device import and distribution.

Data Source and Method Notes

- Primary data: EDE Drug Directory (

services.ede.gov.ae/drugdirectory), medical-device-only extract dated 2026-06-05. The full register contains 16,939 product rows; the medical device subset comprises 4,793 rows. - Analysis: MedDeviceGuide analysis of the EDE public-register extract. All figures are computed directly from the dataset.

- Registration count methodology: Each row represents a unique product-pack-size combination. A single device model registered in multiple pack sizes counts as multiple registrations. This inflates absolute counts relative to distinct device models but accurately reflects the channel and supply-chain burden on suppliers.

- Country of origin: Reflects the manufacturer's declared country, which may be a contract manufacturing site rather than the brand's corporate headquarters. For example, some US-branded contact lenses are manufactured in Ireland, and some European-branded gloves are manufactured in Malaysia.

- Limitations: The EDE register does not include device risk classification (Class I–IV) at the row level — all rows carry the generic "Medical Devices for Humans" label. Analysis by risk class was therefore not possible. The register also does not include separate "authorized representative" or "local agent" fields; the "Supplier Name" field is the closest proxy for the entity holding the market authorization.

Data source: EDE Drug Directory, extracted 2026-06-05. Analysis by MedDeviceGuide. Market size figures from Fortune Business Insights (2026) and industry reports cited above. Regulatory framework details from RegDesk (January 2026), OMC Medical (2026), and MedDeviceGuide's own UAE EDE registration guide.