Qatar's 2,623 Implantable Devices: 62% in 20 Suppliers, Lebanese Lock-In

Qatar MoPH implantable device register: 2,623 devices, 171 suppliers, top 20 control 62%. Lebanese distributor dominance and single-supplier manufacturer lock-in analyzed.

Executive Summary

Qatar's Ministry of Public Health (MoPH) maintains a dedicated registry for implantable medical devices — high-risk products including orthopedic implants, cardiac stents, intraocular lenses, surgical mesh, and neuromodulation systems. Unlike the broader medical device registration process, the implantable device register provides a focused view of the highest-risk segment of Qatar's medical device market.

Our analysis of the MoPH implantable device register (extracted 5 June 2026, 2,623 device entries) reveals an extremely concentrated distribution channel: 171 suppliers manage 2,623 devices from 336 manufacturers, but the top 20 suppliers control 62.0% of all listings. The market is dominated by Lebanese-registered distributors (many with S.A.L. or S.A.R.L. suffixes), and a striking number of major manufacturers — including Smith & Nephew, Zimmer, DePuy (J&J), and Arthrex — are represented by a single sole supplier, creating significant channel lock-in risk.

This article maps the supplier landscape, quantifies the manufacturer-supplier dependencies, and offers practical implications for manufacturers evaluating Qatar market entry or considering channel diversification.

Data Source and Method

- Source: Qatar Ministry of Public Health (MoPH), Implantable Medical Devices Registration Mechanism — public register of registered implantable devices

- Analysis sample: Qatar MoPH implantable-device public register extract dated 5 June 2026 (2,623 rows)

- Fields: supplier_name, manufacturer, commercial_name, registration_code, generic_name, catalogue_numbers, certifications, risk_class, moph_approval_date, source_pdf

- Analysis date: 6 June 2026

- Computed using: MedDeviceGuide analysis of the MoPH public register extract

- Limitations: The register covers implantable devices specifically. Non-implantable Class III devices are registered separately and are not included in this analysis. Supplier names are as recorded in the MoPH register and may not reflect corporate group structures.

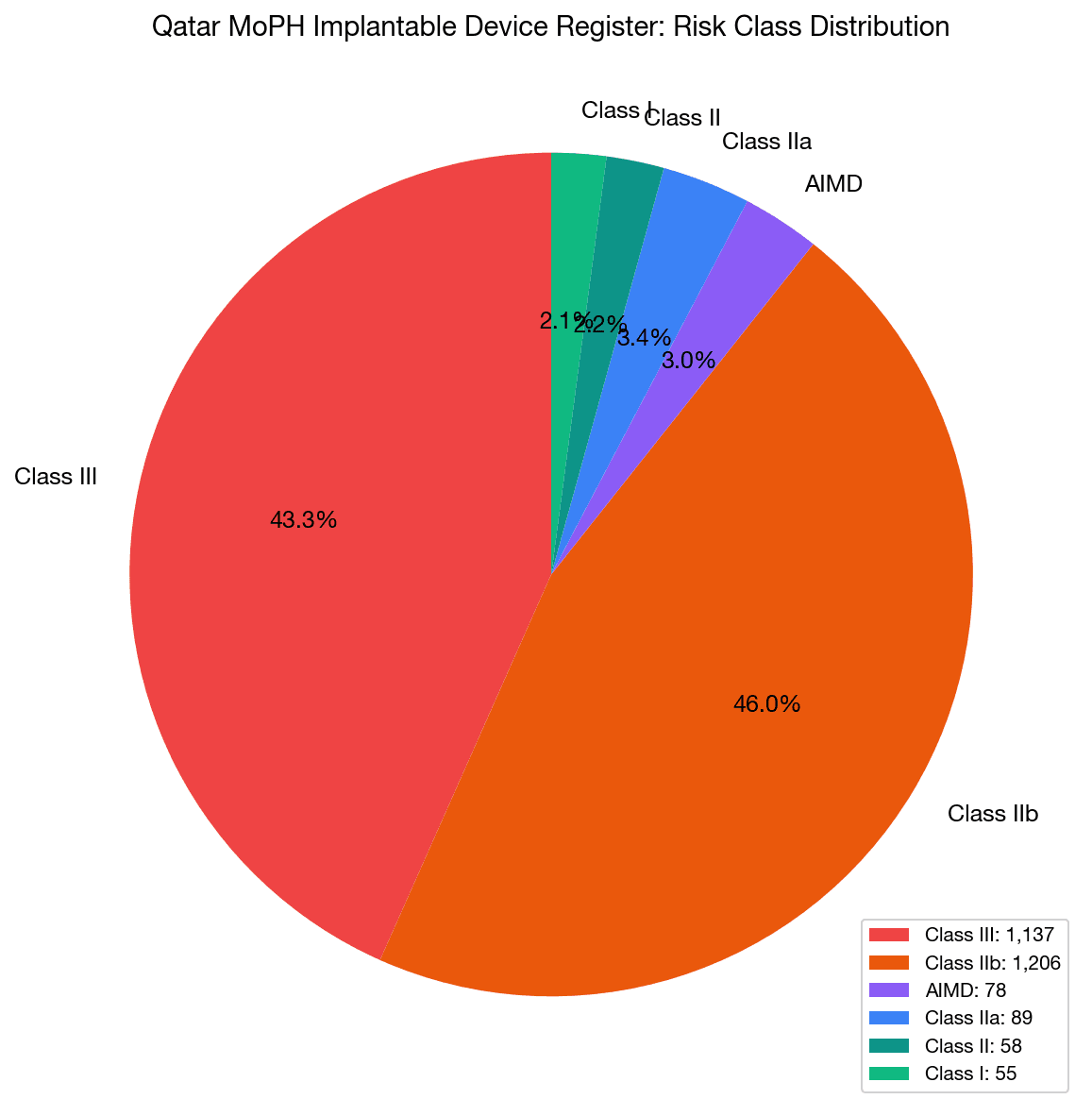

Risk Class Distribution

| Risk Class | Devices | Share |

|---|---|---|

| Class III | 1,137 | 43.3% |

| Class IIb | 1,206 | 46.0% |

| AIMD (Active Implantable) | 78 | 3.0% |

| Class IIa | 89 | 3.4% |

| Class II | 58 | 2.2% |

| Class I | 55 | 2.1% |

89.3% of registered implantable devices are Class IIb or III — consistent with the expected risk profile for implantable products. The presence of 78 AIMD (Active Implantable Medical Device) entries reflects cardiac pacemakers, defibrillators, and neurostimulators. The small Class I and II components (4.3% combined) likely include some surgical accessories and materials classified as implantable-adjacent by the MoPH.

The risk class distribution follows the EU MDR classification framework, consistent with Qatar's regulatory approach of referencing EU classification standards for medical device registration.

Supplier Concentration

The Numbers

| Metric | Value |

|---|---|

| Total device entries | 2,623 |

| Unique suppliers | 171 |

| Unique manufacturers | 336 |

| Devices per supplier (median) | ~5 |

| Suppliers with 1 device | 39 (22.8%) |

The 2,623 devices are distributed across 171 suppliers and 336 manufacturers — meaning the average manufacturer is represented by only 1-2 suppliers, and the average supplier carries about 15 devices.

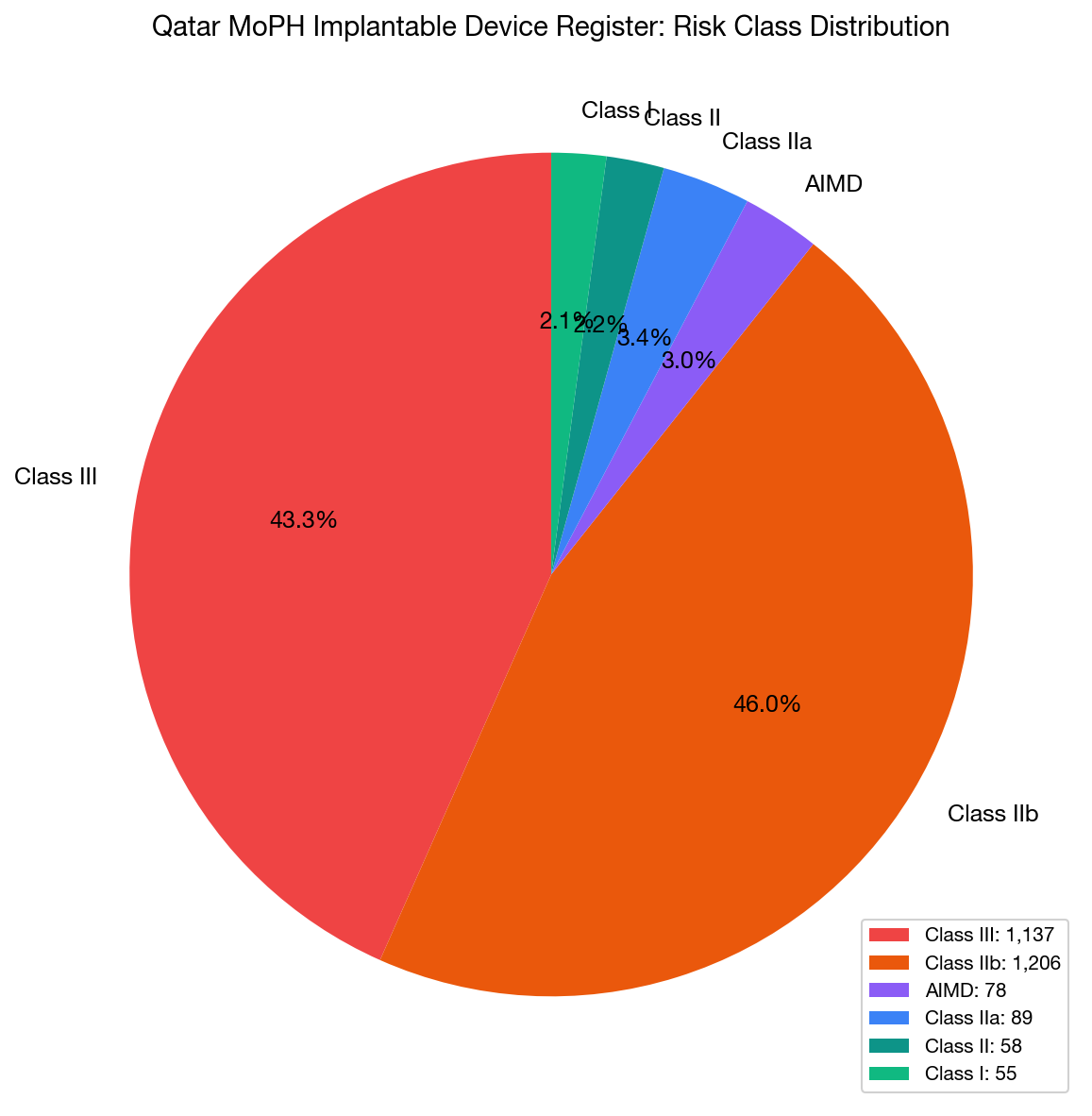

Top 20 Suppliers

| Rank | Supplier | Devices | Share | Manufacturers |

|---|---|---|---|---|

| 1 | Asmar Medical s.a.l | 244 | 9.3% | 17 |

| 2 | Biomedic S.A.L | 146 | 5.6% | 16 |

| 3 | Khalil Fattal et Fils S.A.L | 133 | 5.1% | 6 |

| 4 | Apex Medical | 126 | 4.8% | 5 |

| 5 | DIMA HEALTHCARE SA | 113 | 4.3% | 7 |

| 6 | INTERMEDIC S.A.L | 110 | 4.2% | 5 |

| 7 | Sater Medical Care | 108 | 4.1% | 8 |

| 8 | Arthroleb SAL | 98 | 3.7% | 7 |

| 9 | Tamer Frères S.A.L | 69 | 2.6% | 3 |

| 10 | Promed Technology | 68 | 2.6% | 7 |

| 11 | Sterimed International SAL | 56 | 2.1% | 6 |

| 12 | Biomedic S.A.R.L | 50 | 1.9% | 8 |

| 13 | OrthoSpine SAL | 44 | 1.7% | 9 |

| 14 | Mediline | 42 | 1.6% | 3 |

| 15 | Pragmatic Transparent Solutions SAL | 40 | 1.5% | 12 |

| 16 | Prodent | 40 | 1.5% | 7 |

| 17 | Hi-Tech Gates S.A.R.L | 37 | 1.4% | 6 |

| 18 | Rasamny Health Care Group sal | 36 | 1.4% | 3 |

| 19 | Kaddoum Medical Care S.A.L | 34 | 1.3% | 4 |

| 20 | THE UNICORN s.a.l | 33 | 1.3% | 5 |

Top 20 cumulative: 1,627 devices (62.0%)

The Lebanese Connection

A striking feature of the supplier landscape is the dominance of Lebanese-registered companies. Of the top 20 suppliers, at least 14 carry Lebanese corporate designations (S.A.L. — Société Anonyme Libanaise, or S.A.R.L. — Société à Responsabilité Limitée). This reflects a well-established pattern in the broader Middle East medical device distribution market, where Lebanese trading houses have built extensive regional networks spanning the Levant, GCC, and North Africa.

The top 4 suppliers — Asmar Medical, Biomedic, Khalil Fattal, and Apex Medical — collectively hold 549 devices (20.9%). These firms operate as regional distribution hubs, representing multiple international manufacturers across the MENA region.

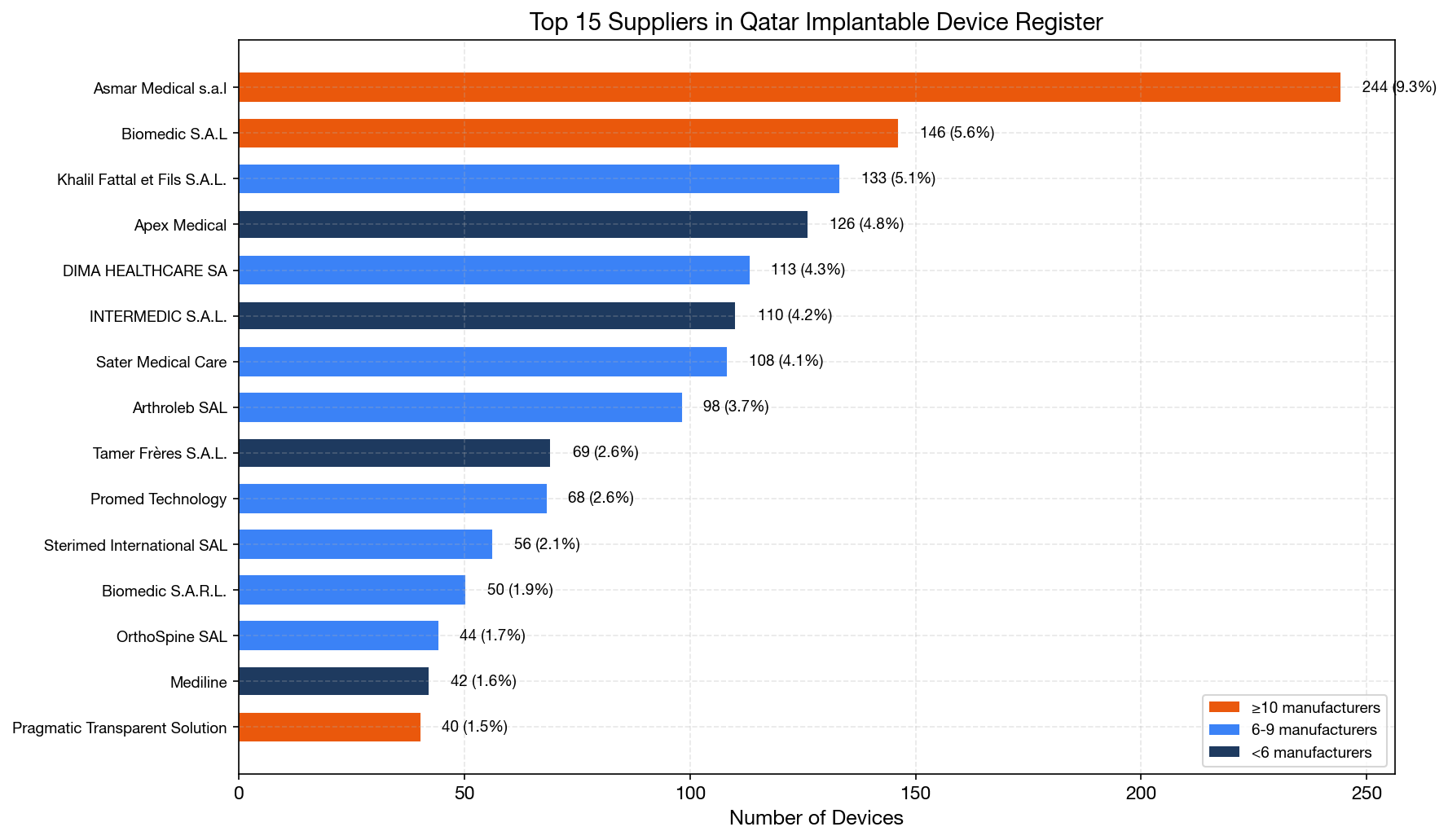

Supplier Concentration Curve

The concentration curve shows that Qatar's implantable device market is significantly more concentrated than a comparable-size European market. The top 10% of suppliers (17 companies) control approximately 75% of all devices, while the bottom 50% hold less than 5%.

Manufacturer Landscape

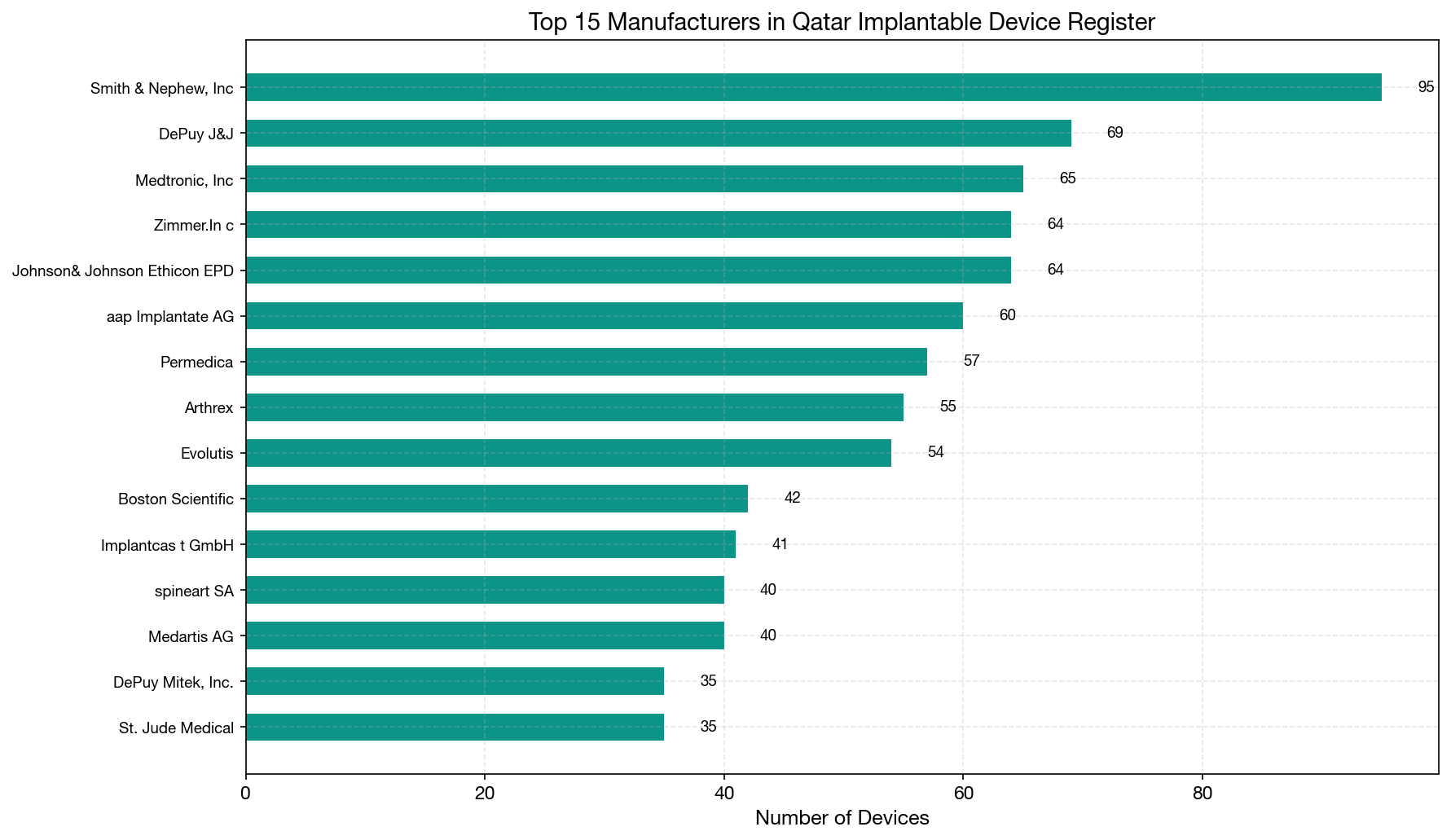

Top 15 Manufacturers

| Rank | Manufacturer | Devices | Share | Suppliers |

|---|---|---|---|---|

| 1 | Smith & Nephew, Inc | 95 | 3.6% | 1 |

| 2 | DePuy (J&J) | 69 | 2.6% | 1 |

| 3 | Medtronic, Inc | 65 | 2.5% | 2 |

| 4 | Zimmer Inc | 64 | 2.4% | 1 |

| 5 | Johnson & Johnson Ethicon EPD | 64 | 2.4% | 1 |

| 6 | aap Implantate AG | 60 | 2.3% | 1 |

| 7 | Permedica | 57 | 2.2% | 2 |

| 8 | Arthrex | 55 | 2.1% | 1 |

| 9 | Evolutis | 54 | 2.1% | 2 |

| 10 | Boston Scientific | 42 | 1.6% | 4 |

| 11 | Implantcast GmbH | 41 | 1.6% | 1 |

| 12 | spineart SA | 40 | 1.5% | 1 |

| 13 | Medartis AG | 40 | 1.5% | 3 |

| 14 | DePuy Mitek, Inc | 35 | 1.3% | 1 |

| 15 | St. Jude Medical | 35 | 1.3% | 2 |

The manufacturer list reads as a who's who of the global orthopedic, cardiovascular, and surgical implant industry. Smith & Nephew leads with 95 devices, followed by DePuy/J&J entities (DePuy + DePuy Mitek + Ethicon EPD = 168 combined devices across the J&J family).

Notably, the manufacturer field shows no overlap with the supplier field — no manufacturer also appears as its own supplier in the register. This confirms that the MoPH requires a clear separation between the manufacturing entity and the local supplier/distributor.

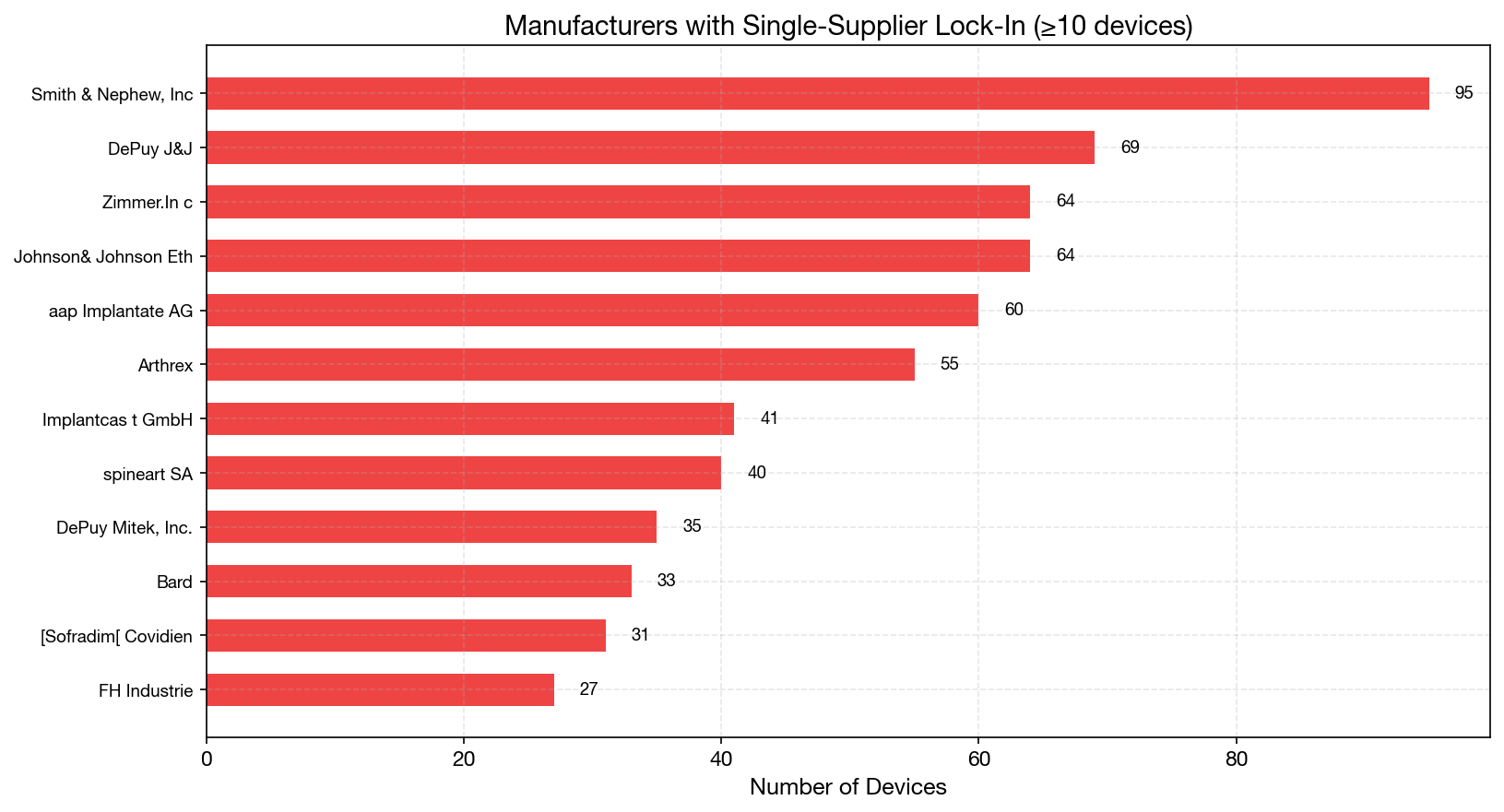

Channel Lock-In: Manufacturers with a Single Supplier

A critical finding is the prevalence of single-supplier manufacturer relationships. Of the 336 manufacturers in the register, a large number are represented by exactly one supplier. For manufacturers with 10 or more device registrations, the following are sole-sourced:

| Manufacturer | Devices | Sole Supplier |

|---|---|---|

| Smith & Nephew, Inc | 95 | Khalil Fattal et Fils S.A.L |

| DePuy (J&J) | 69 | Asmar Medical s.a.l |

| Zimmer Inc | 64 | Biomedic S.A.L |

| Johnson & Johnson Ethicon EPD | 64 | INTERMEDIC S.A.L |

| aap Implantate AG | 60 | Apex Medical |

| Arthrex | 55 | Arthroleb SAL |

| Implantcast GmbH | 41 | Sater Medical Care |

| spineart SA | 40 | Apex Medical |

| DePuy Mitek, Inc | 35 | Asmar Medical s.a.l |

| Bard | 33 | Mediline |

| Sofradim/Covidien | 31 | DIMA HEALTHCARE SA |

| FH Industrie | 27 | Promed Technology |

| Groupe Lepine | 26 | Sterimed International SAL |

| Covidien | 25 | DIMA HEALTHCARE SA |

| GRUPPO BIOIMPIANTI | 24 | Arthroleb SAL |

This is a significant finding for several reasons:

Switching costs are high: Changing the local supplier for an implantable device requires MoPH notification, updated registration documentation, and potentially re-approval. This creates a high-friction barrier to channel changes.

Supply chain risk: For manufacturers like Smith & Nephew (95 devices through a single supplier) or Zimmer (64 devices through a single supplier), any disruption to the supplier relationship — whether commercial, financial, or regulatory — could effectively remove their entire Qatar product portfolio from the market.

Negotiating leverage: The sole-supplier structure gives the distributor significant leverage over pricing, terms, and market access decisions. Manufacturers entering new product categories in Qatar should consider multi-supplier strategies from the outset.

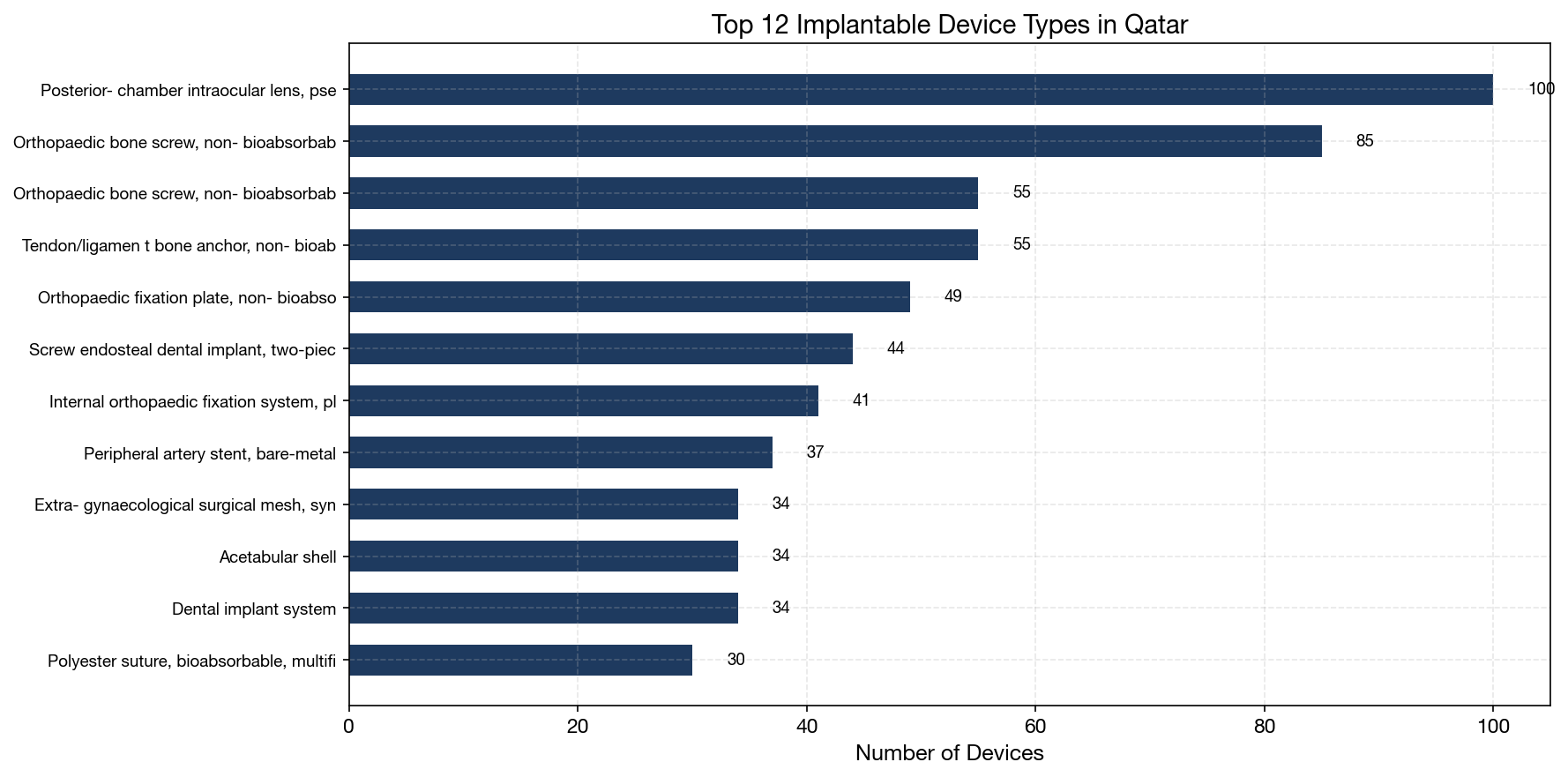

Device Type Distribution

The most common implantable device types registered with MoPH:

| Device Type | Count | Share |

|---|---|---|

| Posterior-chamber intraocular lens | 100 | 3.8% |

| Orthopedic bone screw (non-bioabsorbable) | 140 | 5.3% |

| Tendon/ligament bone anchor | 55 | 2.1% |

| Orthopedic fixation plate | 76 | 2.9% |

| Screw endosteal dental implant | 44 | 1.7% |

| Internal orthopedic fixation system | 41 | 1.6% |

| Peripheral artery stent (bare-metal) | 37 | 1.4% |

| Surgical mesh (synthetic, non-bioabsorbable) | 34 | 1.3% |

| Acetabular shell | 34 | 1.3% |

| Dental implant system | 34 | 1.3% |

Orthopedic implants (screws, plates, fixation systems, anchors) collectively represent the largest device category, followed by ophthalmic implants (intraocular lenses) and dental implants. The vascular segment is represented by peripheral artery stents (37 devices) and cardiac rhythm management devices (within the AIMD category).

Practical Implications for Manufacturers

1. Qatar's Small Market Size Demands Efficient Channel Design

With only 2,623 registered implantable devices, Qatar is a small market by volume. The MoPH's regulatory requirements — including ISO 13485 certification, Certificate of Free Sale, bilingual (English/Arabic) labeling, and implantable-specific registration documentation — create a compliance overhead that must be amortized across relatively few units. Choosing a regional distributor who already operates in Qatar can spread compliance costs across multiple product lines and markets.

2. Evaluate Regional Distributors, Not Just Qatar Specialists

The dominance of Lebanese regional distributors is not accidental — these firms provide coverage across the Levant, GCC, and often North Africa. For manufacturers seeking broader Middle East market access, partnering with a distributor already established in Qatar offers a pathway to multi-market expansion. However, verify that the distributor has dedicated Qatar regulatory capabilities, as the MoPH has specific documentation and language requirements.

3. Multi-Supplier Strategy Reduces Lock-In Risk

For manufacturers with large product portfolios, consider splitting the portfolio across two or more suppliers. This reduces channel lock-in, creates competitive dynamics, and provides a fallback if one supplier faces regulatory or financial difficulties. The MoPH register shows that some manufacturers (e.g., Boston Scientific with 4 suppliers, Medartis AG with 3 suppliers) already follow this approach.

4. Leverage Reference Market Approvals

Qatar's MoPH accepts registrations supported by approvals from reference regulators, including US FDA, EU CE marking, and Saudi SFDA. Manufacturers with existing approvals from these authorities can streamline the Qatar registration process by submitting their conformity assessment documentation. The certifications field in the MoPH register shows extensive use of FDA Certificates for Foreign Government (CFG), EU Quality Management System certificates, and EU Free Sale Certifications as supporting evidence.

5. Post-Market Obligations Should Not Be Overlooked

Implantable devices carry enhanced post-market requirements in Qatar, including adverse event reporting, product recall procedures, and traceability obligations. Ensure that the appointed supplier has the infrastructure and willingness to manage these obligations, including maintaining the required records of implantation and explantation at Qatari healthcare facilities.

Context and Regulatory Framework

Qatar's Ministry of Public Health (MoPH) regulates medical devices under the Implantable Medical Devices Registration Mechanism, which requires all healthcare facilities to register the implantable devices they use. The framework references the EU MDR classification system and requires:

- ISO 13485 certification for manufacturers

- Certificate of Free Sale (CFS) from the country of origin

- Technical documentation and conformity assessment evidence

- Instructions for use in both English and Arabic

- Registration of supplier, manufacturer, and device details with the MoPH

Qatar is part of the Gulf Cooperation Council (GCC) health regulatory environment, alongside Saudi Arabia, UAE, Kuwait, Bahrain, and Oman. While there is no centralized GCC medical device registration (unlike pharmaceuticals through the Gulf Health Council), approvals from reference markets — particularly Saudi SFDA — can facilitate the Qatar registration process.

Summary

| Metric | Value |

|---|---|

| Registered implantable devices | 2,623 |

| Unique suppliers | 171 |

| Unique manufacturers | 336 |

| Top 20 supplier concentration | 62.0% |

| Devices in Class IIb + III | 89.3% |

| Lebanese-registered top suppliers | ~14 of top 20 |

| Manufacturers with sole supplier (≥10 devices) | 15 |

| Top supplier | Asmar Medical s.a.l (244 devices, 9.3%) |

| Top manufacturer | Smith & Nephew, Inc (95 devices, 3.6%) |

Qatar's implantable device market is small but structurally concentrated, with regional distributors — particularly Lebanese firms — controlling the majority of market access. Manufacturers should approach Qatar as part of a broader GCC strategy, evaluate multi-supplier options to reduce lock-in risk, and leverage reference market approvals to streamline the registration process.