Mexico COFEPRIS Registration Holders: 5,286 Holders and the 2024 Volume Surge

Analysis of Mexico's 16,473 COFEPRIS registrations reveals 5,286 holders, 60% single-registration, diagnostics dominance at 37%, and a 2024 record peak.

Executive Summary

Mexico's Comisión Federal para la Protección contra Riesgos Sanitarios (COFEPRIS) requires medical device manufacturers — whether domestic or foreign — to obtain a health registration (registro sanitario) through a local entity known as the Mexico Registration Holder (MRH). The MRH is a Mexican legal entity responsible for submitting and maintaining the registration before COFEPRIS.

Our analysis of 16,473 COFEPRIS medical device registrations (extracted from publicly available registration PDFs covering 2017-2025) reveals a highly fragmented landscape: 5,286 unique registration holders, of which 3,174 (60.0%) hold only a single registration. The top 20 holders collectively control just 17.0% of registrations — far less concentrated than comparable markets like Saudi Arabia or Australia.

At the same time, 2024 saw a record 3,556 new registrations (21.6% of the total dataset), likely reflecting both genuine market growth and COFEPRIS's regulatory modernization efforts, including the new Abbreviated Regulatory Pathway effective September 2025. Diagnostic agents dominate at 37% of all registrations, and the data reveals a distinctive class distribution skewed toward Class I and II devices.

This article presents the data, the holder dynamics, and the practical implications for manufacturers evaluating MRH selection and market entry timing.

Data Source and Method

- Source: COFEPRIS public registration database, extracted from PDFsanitary registrations published on the COFEPRIS portal

- Analysis samples:

- COFEPRIS registration extract dated 5 June 2026 (18,037 raw rows, 16,473 after deduplication and cleaning)

- COFEPRIS holder summary extract dated 5 June 2026 (5,286 holder summary rows)

- Time range: 2017-2025

- Analysis date: 6 June 2026

- Computed using: MedDeviceGuide analysis of COFEPRIS public extracts

- Limitations: Category and class labels were extracted from PDFs and exhibit significant formatting inconsistencies (e.g., "Clase I", "CLASE I", "I- BAJO RIESGO" all map to Class I). Normalized classifications are presented alongside raw counts. The dataset may not capture all low-risk notifications that do not require full registration.

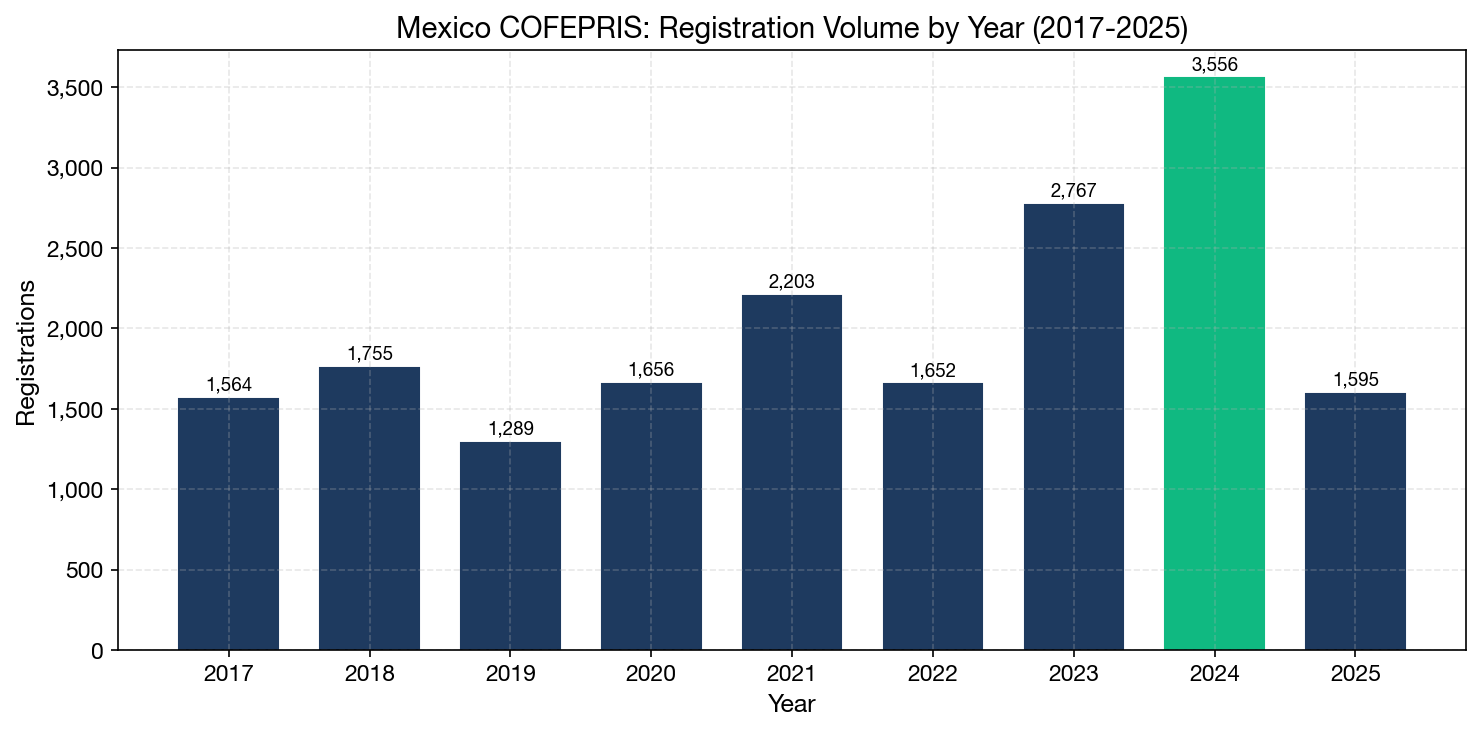

Registration Volume Trend (2017-2025)

| Year | Registrations | Share |

|---|---|---|

| 2017 | 1,564 | 9.5% |

| 2018 | 1,755 | 10.7% |

| 2019 | 1,289 | 7.8% |

| 2020 | 1,656 | 10.1% |

| 2021 | 2,203 | 13.4% |

| 2022 | 1,652 | 10.0% |

| 2023 | 2,767 | 16.8% |

| 2024 | 3,556 | 21.6% |

| 2025 (partial) | 1,595 | 9.7% |

Registration volume has trended upward, with 2024 recording the highest volume in the dataset at 3,556 registrations — more than double the 2019 trough of 1,289. The 2020 dip (likely COVID-related) was followed by a strong recovery. The 2025 figure of 1,595 is partial (data extracted mid-year), suggesting the full-year total may approach or exceed 2024 levels.

This growth trajectory aligns with COFEPRIS's regulatory modernization agenda. The agency has been actively reforming its medical device registration framework, including the introduction of the Abbreviated Regulatory Pathway effective September 1, 2025, which recognizes prior approvals from IMDRF and MDSAP member authorities with a mandated 30-day decision timeline. This fast-track route is expected to further accelerate registration volumes from 2026 onward.

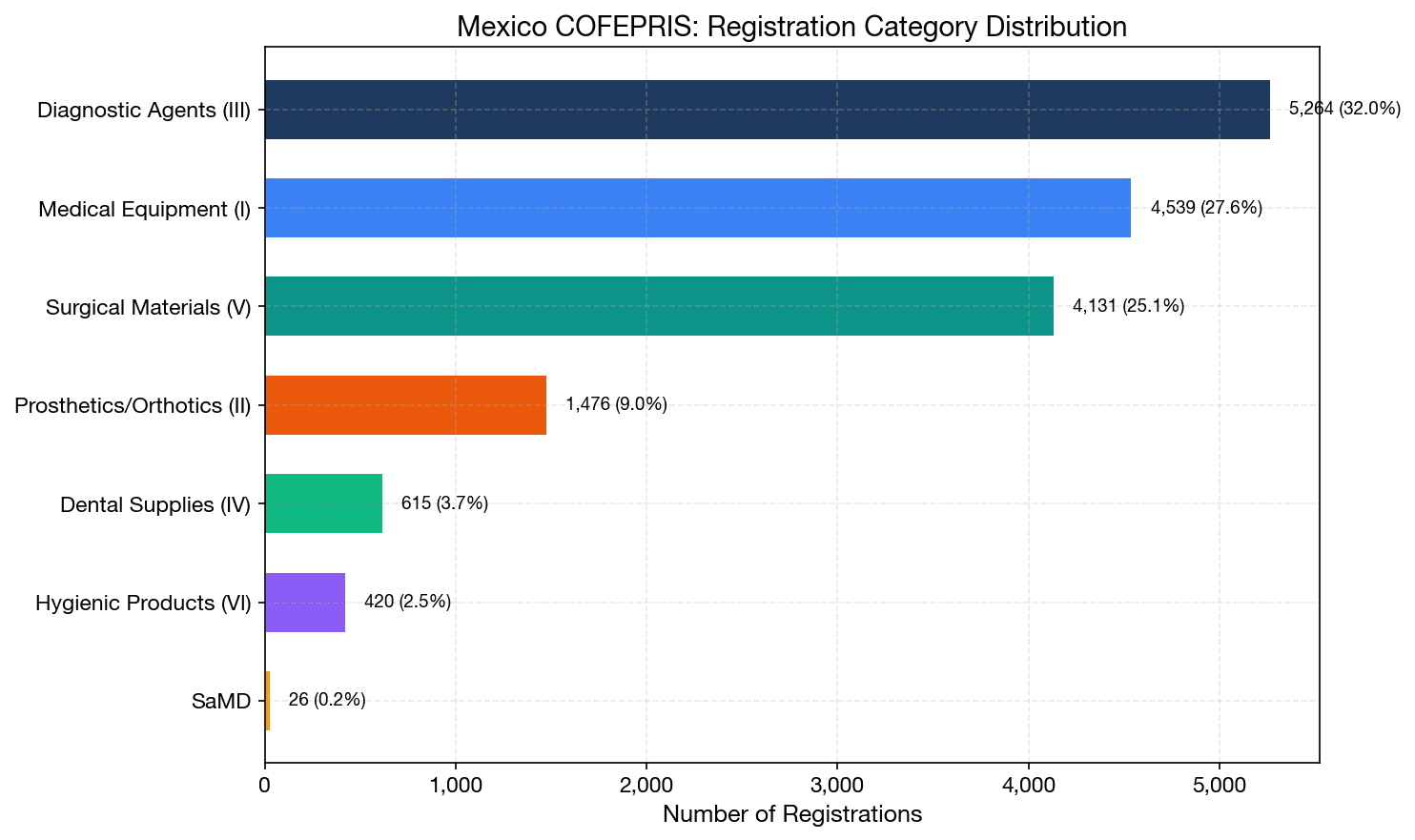

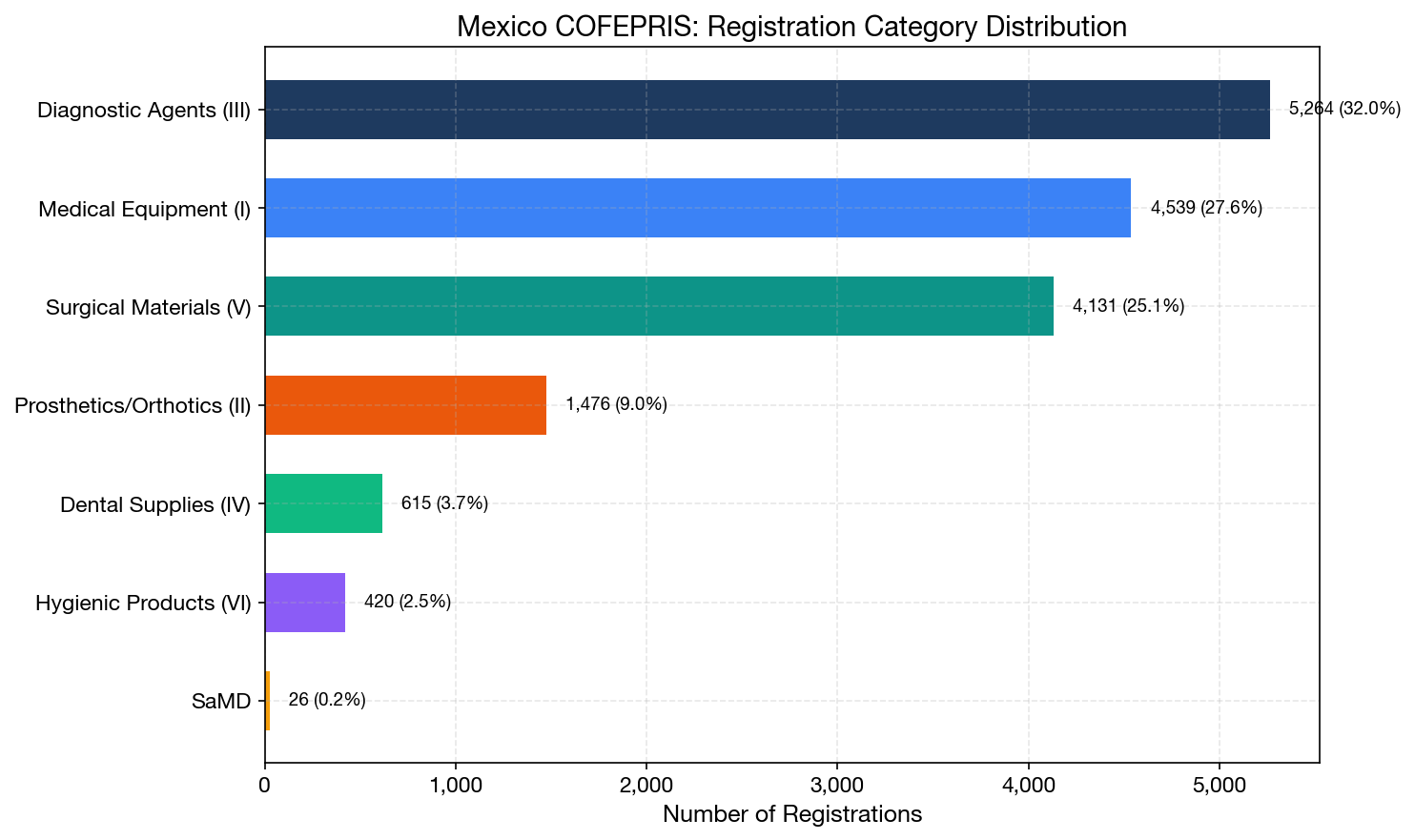

Category Distribution

After normalizing the varied PDF-extracted category labels, the registration distribution is:

| Normalized Category | Registrations | Share |

|---|---|---|

| Diagnostic Agents (Cat. III) | 6,094 | 37.0% |

| Medical Equipment (Cat. I) | 4,504 | 27.3% |

| Surgical Materials (Cat. V) | 3,809 | 23.1% |

| Prosthetics & Orthotics (Cat. II) | 1,502 | 9.1% |

| Dental Supplies (Cat. IV) | 707 | 4.3% |

| Hygienic Products (Cat. VI) | 425 | 2.6% |

Diagnostic agents dominate at 37.0% — a striking proportion that reflects Mexico's growing IVD market and the country's role as a diagnostic manufacturing and distribution hub for Latin America. Combined with Medical Equipment (27.3%), these two categories account for nearly two-thirds of all registrations.

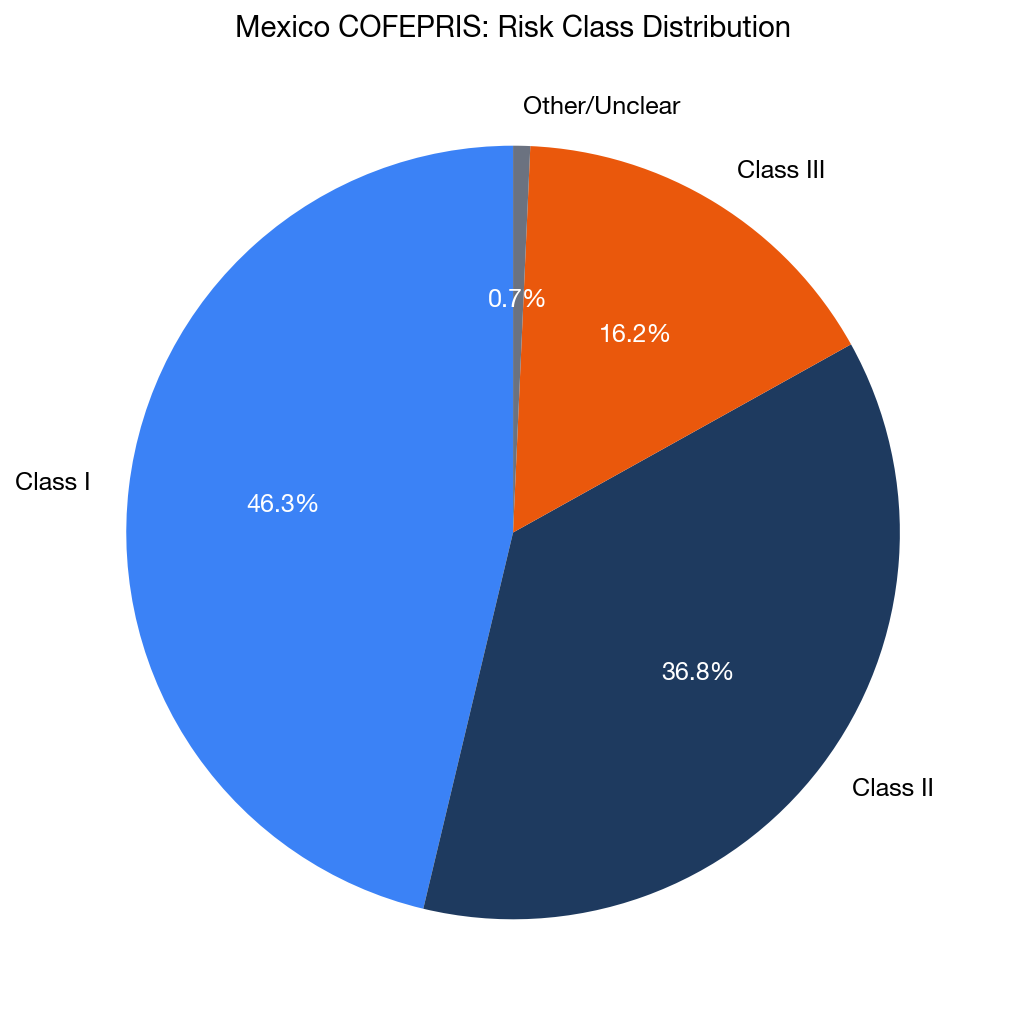

Risk Class Distribution

| Normalized Class | Registrations | Share |

|---|---|---|

| Class I (low risk) | 6,602 | 40.1% |

| Class II (moderate risk) | 6,322 | 38.4% |

| Class III (high risk) | 2,756 | 16.7% |

| Other/Unclear | 793 | 4.8% |

Class I and II devices together represent 78.5% of registrations, consistent with most medical device markets where lower-risk devices vastly outnumber high-risk ones. The 16.7% Class III share is notable — higher than in some comparable markets — and may reflect Mexico's strong surgical and interventional device market.

Category × Risk Class Matrix

The intersection of category and class reveals important patterns:

| Category | Class I | Class II | Class III |

|---|---|---|---|

| Diagnostic Agents | 3,998 | 1,609 | 50 |

| Medical Equipment | 1,369 | 2,652 | 336 |

| Surgical Materials | 1,516 | 1,479 | 768 |

| Prosthetics & Orthotics | 74 | 148 | 1,147 |

| Dental Supplies | 124 | 438 | 30 |

| Hygienic Products | 124 | 216 | 2 |

Key observations:

- Diagnostic agents are overwhelmingly Class I and II (99.2%), reflecting the IVD product mix of reagents, test kits, and instruments.

- Prosthetics & Orthotics are overwhelmingly Class III (76.4%), as expected for implantable devices.

- Surgical Materials span all three classes, with the highest Class III share (20.2%) among the high-volume categories.

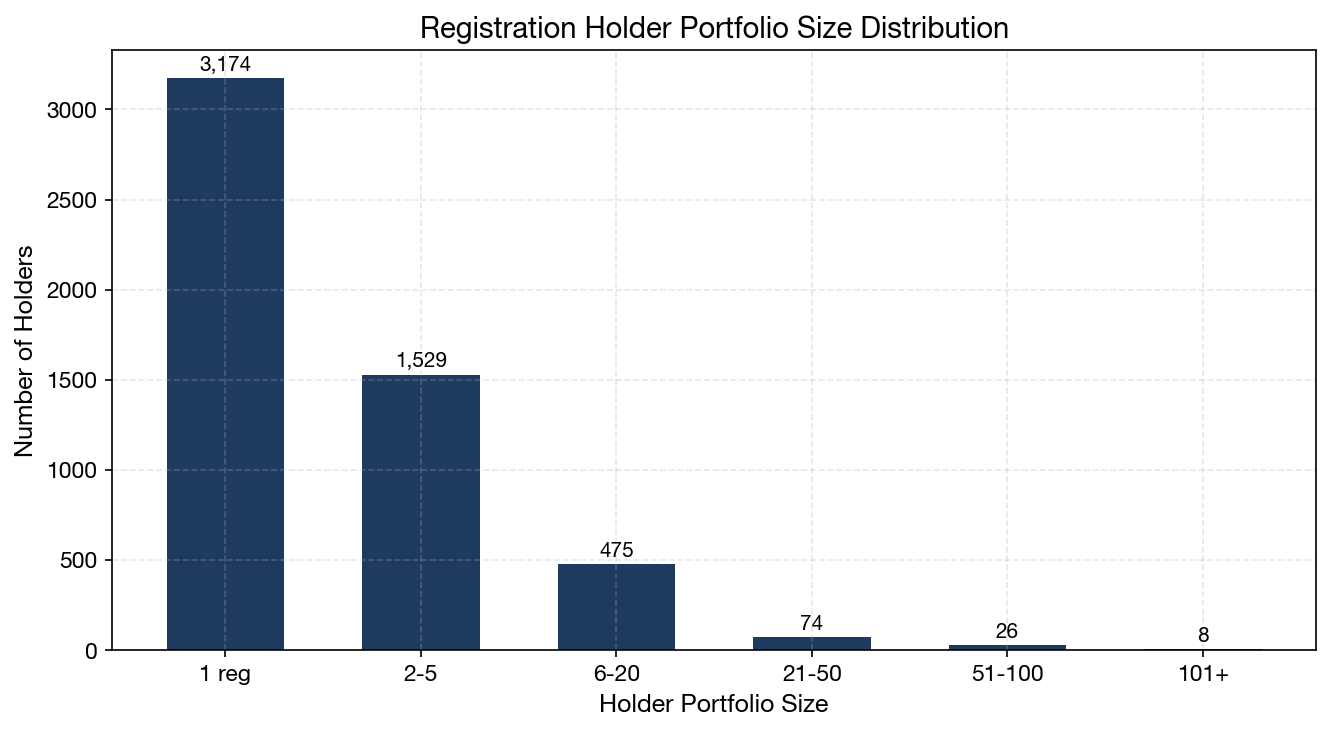

Registration Holder Concentration

Portfolio Size Distribution

| Holder Portfolio Size | Number of Holders | % of Holders |

|---|---|---|

| 1 registration | 3,174 | 60.0% |

| 2-5 registrations | 1,245 | 23.6% |

| 6-20 registrations | 538 | 10.2% |

| 21-50 registrations | 188 | 3.6% |

| 51-100 registrations | 72 | 1.4% |

| 101+ registrations | 69 | 1.3% |

60% of all holders have only a single registration — a remarkably fragmented market. This is significantly higher than the 23% single-device AR rate we observed in Saudi Arabia, suggesting that many Mexican registration holders are either single-product importers, local distributors with limited portfolios, or captive entities set up by a single foreign manufacturer.

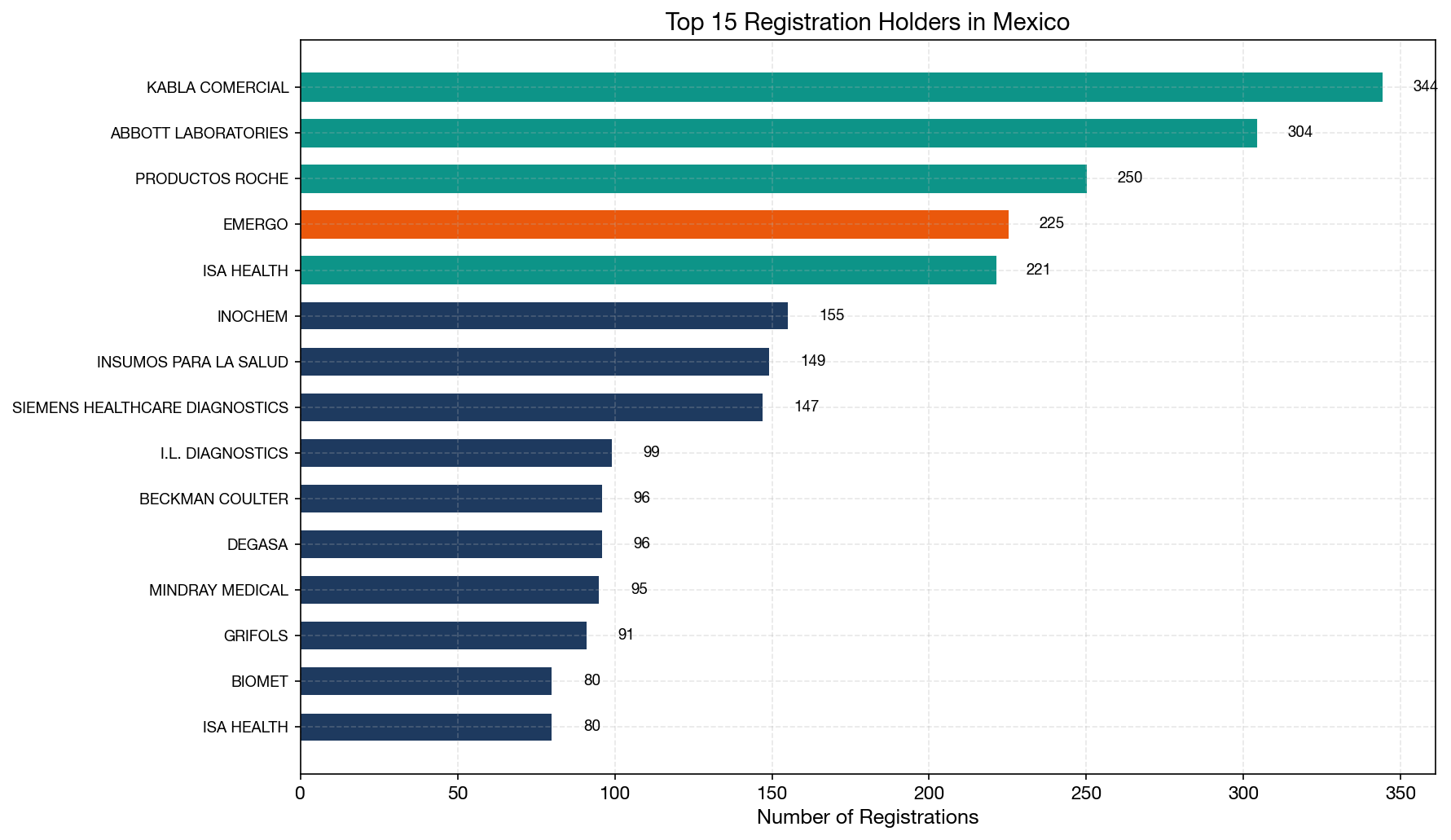

Top 20 Registration Holders

| Rank | Holder | Registrations | Share | Primary Category |

|---|---|---|---|---|

| 1 | KABLA COMERCIAL | 344 | 2.1% | Diagnostic Agents |

| 2 | ABBOTT LABS DE MÉXICO | 304 | 1.8% | Diagnostic Agents |

| 3 | PRODUCTOS ROCHE | 250 | 1.5% | Diagnostic Agents |

| 4 | EMERGO S. DE R.L. DE C.V | 225 | 1.4% | Mixed |

| 5 | ISA HEALTH | 221 | 1.3% | Diagnostic Agents |

| 6 | INOCHEM | 155 | 0.9% | Diagnostic Agents |

| 7 | INSUMOS PARA LA SALUD | 149 | 0.9% | Diagnostic Agents |

| 8 | SIEMENS HEALTHCARE DIAGNOSTICS | 147 | 0.9% | Diagnostic Agents |

| 9 | I.L. DIAGNOSTICS | 99 | 0.6% | Diagnostic Agents |

| 10 | BECKMAN COULTER DE MÉXICO | 96 | 0.6% | Diagnostic Agents |

| 11 | DEGASA | 96 | 0.6% | Surgical Materials |

| 12 | MINDRAY MEDICAL MÉXICO | 95 | 0.6% | Diagnostic Agents |

| 13 | GRIFOLS MÉXICO | 91 | 0.6% | Diagnostic Agents |

| 14 | BIOMET MÉXICO | 80 | 0.5% | Equipment/Prosthetics |

| 15 | ISA HEALTH (variant) | 80 | 0.5% | Diagnostic Agents |

| 16 | BOSTON SCIENTIFIC DE MÉXICO | 77 | 0.5% | Mixed |

| 17 | JOHNSON & JOHNSON DE MÉXICO | 76 | 0.5% | Mixed |

| 18 | QUIMIBIOL | 74 | 0.4% | Diagnostic Agents |

| 19 | BECKMAN COULTER MÉXICO | 73 | 0.4% | Diagnostic Agents |

| 20 | BECTON DICKINSON DE MÉXICO | 64 | 0.4% | Diagnostic Agents |

Top 20 cumulative: 2,796 registrations (17.0%)

Several patterns stand out:

Diagnostics dominance: 14 of the top 20 holders are primarily diagnostic agents companies. This reflects the highly consolidated IVD distribution market in Mexico, where a handful of importers handle the major global brands (Abbott, Roche, Siemens, Beckman Coulter).

Emergo as a regulatory service provider: Emergo (by UL) is the only pure regulatory-service MRH in the top 20, with 225 registrations across diverse categories. Most other top holders are either manufacturers' local subsidiaries (Abbott, Roche, Siemens, Boston Scientific, J&J, BD) or specialized distributors.

Name variants: The dataset contains name variants for the same entity (e.g., "ISA HEALTH, S.A. DE C.V" and "ISA HEALTH, S.A. C.V"), suggesting the true concentration may be somewhat higher than what the raw data shows.

Low top-holder share: Even the #1 holder (KABLA COMERCIAL) controls only 2.1% of registrations — dramatically lower than the 4.6% top-AR share in Saudi Arabia. This reflects Mexico's more fragmented, distributor-driven market structure.

Practical Implications for Manufacturers

1. Understanding the MRH Landscape

Foreign manufacturers must appoint a Mexico Registration Holder (MRH) — a local legal entity authorized to act on the manufacturer's behalf before COFEPRIS. The MRH holds the registration, manages renewals, and is the official point of contact for regulatory communications. Unlike the Saudi AR system, where some ARs serve as multi-manufacturer hubs, the Mexican market is dominated by manufacturer-specific subsidiaries and specialized distributors.

2. Choose Your MRH Based on Portfolio Strategy

- For IVD manufacturers: The IVD distribution market is highly consolidated. Working with established IVD distributors who already hold registrations for complementary products can provide infrastructure and market access advantages.

- For surgical and implantable device manufacturers: The surgical materials and prosthetics categories are more fragmented, with many smaller holders. Manufacturers should evaluate potential MRHs based on their specific device class and category experience.

- For multi-product manufacturers: Consider whether a single MRH can manage your entire portfolio or whether splitting across specialized holders makes more sense.

3. Leverage the New Abbreviated Pathway

Effective September 2025, COFEPRIS introduced an Abbreviated Regulatory Pathway that recognizes prior approvals from IMDRF and MDSAP member authorities (including US FDA, Health Canada, Japan PMDA, and EU CE marking under MDR). This pathway mandates a 30-day decision timeline — a significant improvement over the standard 6+ month review for Class III devices. Manufacturers with existing approvals from reference authorities should prioritize this route for new Mexican registrations.

4. Plan for Registration Renewal

COFEPRIS registrations have a 5-year validity. The 2021 surge in registrations (2,203, up from 1,289 in 2019) means a significant cohort will come up for renewal in 2026. Manufacturers should ensure their MRH has the capacity and documentation ready for renewal submissions.

5. Budget Realistically for Market Entry

Government fees for COFEPRIS registration are relatively modest compared to many markets, but total costs — including MRH fees, consulting, translation, document preparation, and legalization — typically range from a few thousand dollars for a simple Class I notification to $20,000+ for a complex Class III device through the Standard Route. The Abbreviated Pathway may reduce some of these costs by simplifying documentation requirements.

Context and Regulatory Framework

Mexico's medical device regulatory framework is administered by COFEPRIS under the Ley General de Salud (General Health Law) and its implementing regulations. The classification system follows a risk-based approach with three main classes (I, II, III) and additional subcategories for low-risk devices.

The recent regulatory modernization includes:

- Abbreviated Regulatory Pathway (September 2025): fast-track route recognizing prior foreign approvals, with 30-day decision timeline

- Consolidated registration procedures: simplification combining new registrations, low-risk registrations, and first extension applications into unified procedures

- Digitalization initiatives: ongoing improvements to electronic submission systems

Foreign manufacturers must comply with Mexico's NOM (Norma Oficial Mexicana) standards where applicable, and the MRH is responsible for ensuring ongoing post-market compliance, including adverse event reporting and product vigilance.

Summary

| Metric | Value |

|---|---|

| Registrations analyzed | 16,473 |

| Unique registration holders | 5,286 |

| Holders with 1 registration | 3,174 (60.0%) |

| Top 20 holder concentration | 17.0% |

| Largest category | Diagnostic Agents (37.0%) |

| Peak registration year | 2024 (3,556 registrations) |

| Class I + II share | 78.5% |

| #1 holder | KABLA COMERCIAL (344 registrations, 2.1%) |

The Mexican COFEPRIS market is large, growing, and highly fragmented. The 2024 registration surge and the new Abbreviated Pathway signal increasing accessibility for foreign manufacturers, but the MRH selection decision remains critical — particularly for companies seeking to build a multi-product presence in Mexico's evolving regulatory environment.