FDA 510(k) by Medical Specialty: 8 Panels Control 68% of All Clearances

175,149 FDA 510(k) clearances analyzed by medical specialty: the top 8 panels control 68%, Cardiovascular leads all-time, and Radiology is the fastest-growing as imaging AI reshapes the mix.

Executive Summary

The FDA's 510(k) database is often described as a single pipeline, but the workload is in fact concentrated in a handful of medical specialties. Our analysis of all 175,149 510(k) clearances on record — each tagged to an advisory committee representing a medical specialty — reveals a review landscape dominated by a small number of panels and reshaped by software and imaging:

- The top 8 advisory committees account for 68.1% of every 510(k) clearance ever issued; the top 5 alone account for 47.1%

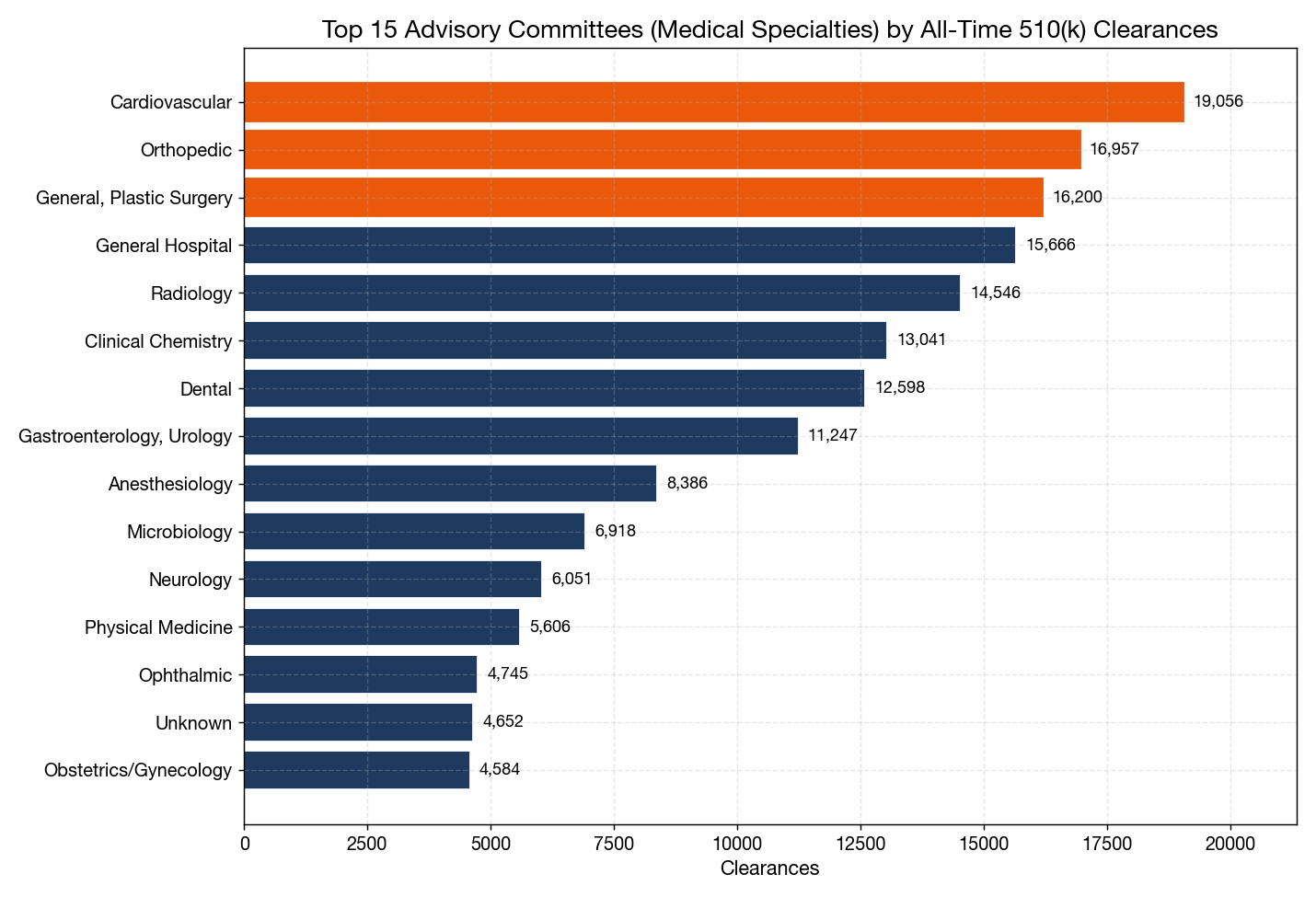

- Cardiovascular leads all-time with 19,056 clearances (10.9%), narrowly ahead of Orthopedic (16,957, 9.7%), General & Plastic Surgery (16,200, 9.2%), General Hospital (15,666, 8.9%), and Radiology (14,546, 8.3%)

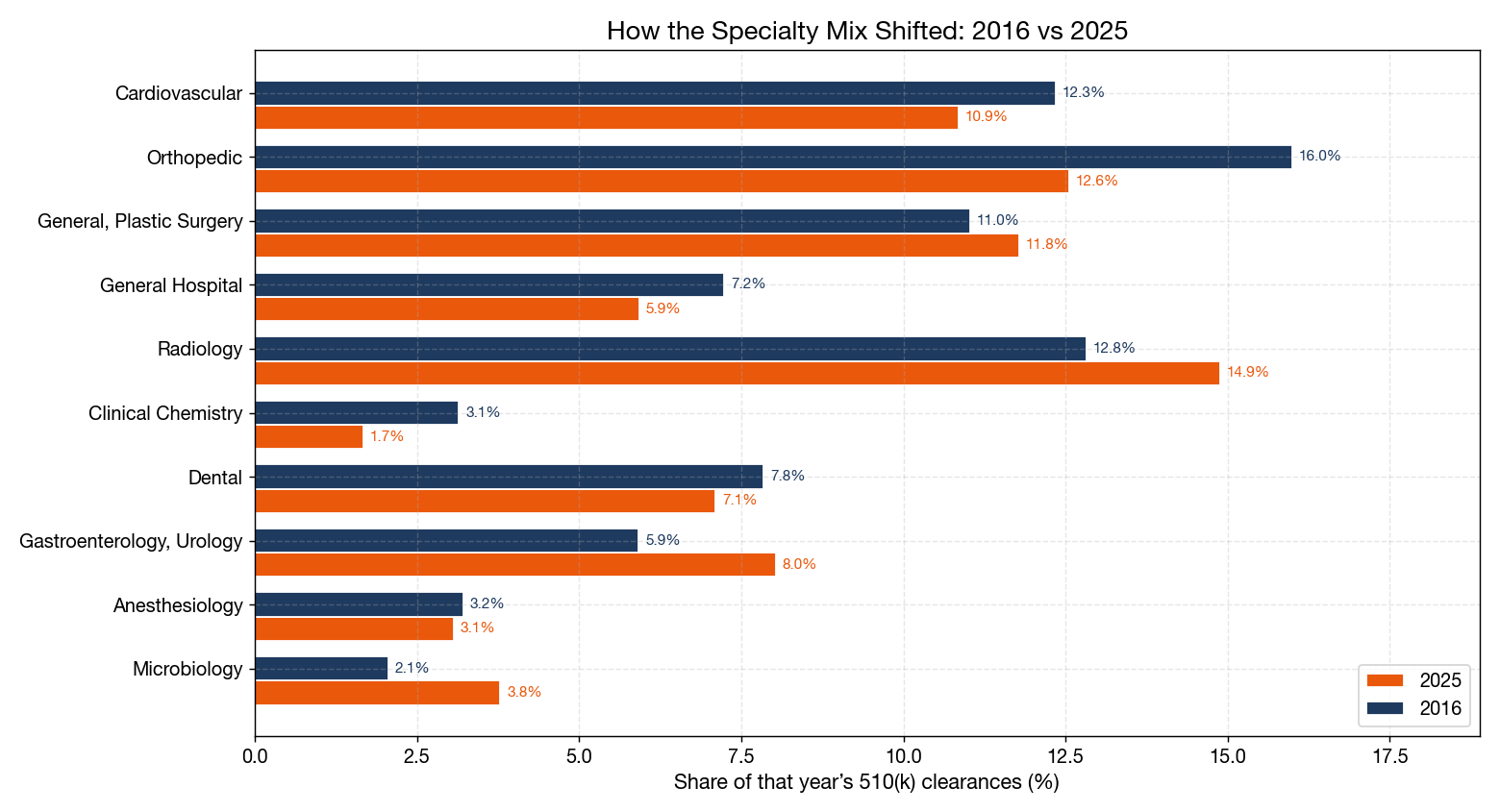

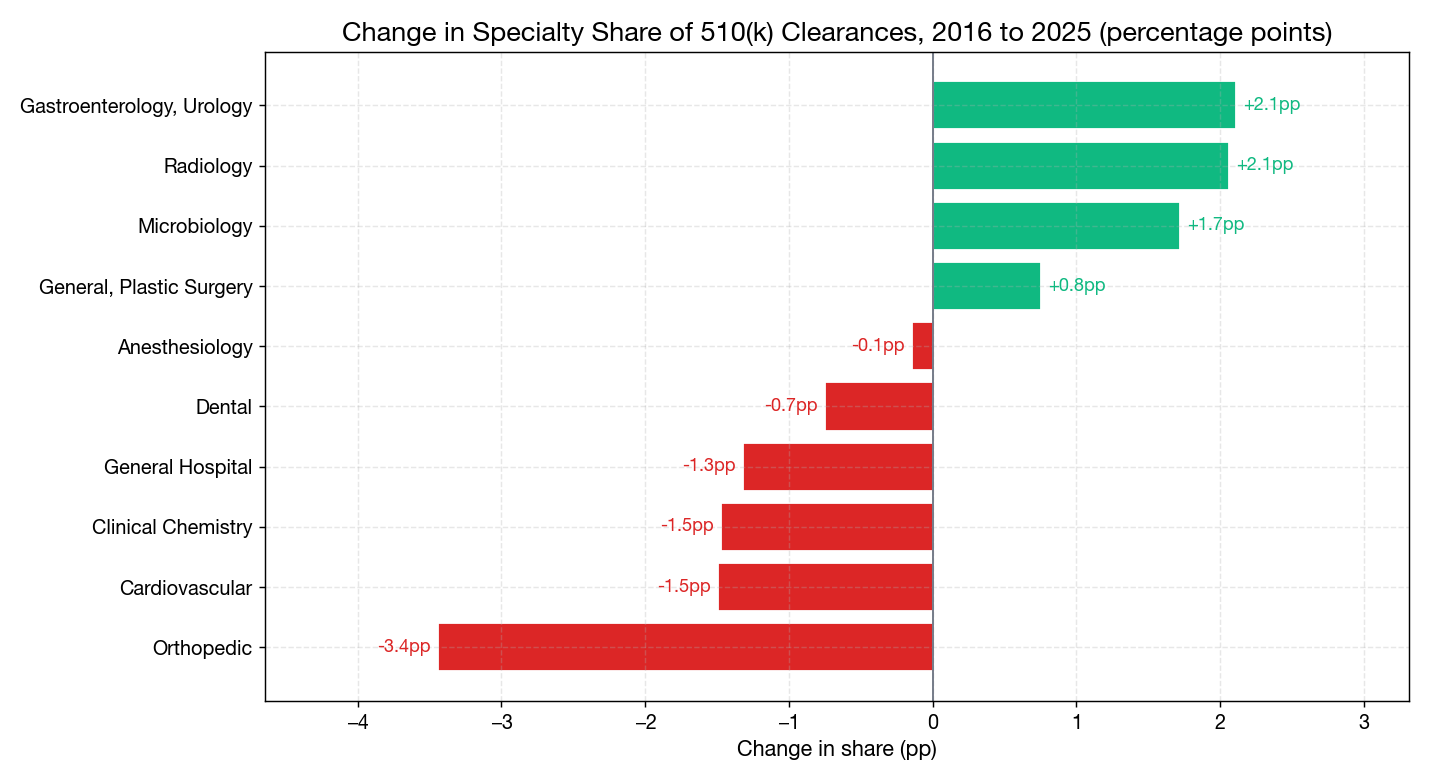

- Radiology is the fastest-growing specialty: its share of annual 510(k) clearances rose from 12.8% in 2016 to 14.9% in 2025 (+2.1 percentage points), driven by the imaging AI boom, while Orthopedic's share fell 3.4 points over the same period

- Microbiology (+1.7pp) and Gastroenterology/Urology (+2.1pp) also gained share, reflecting growth in diagnostics and minimally invasive devices

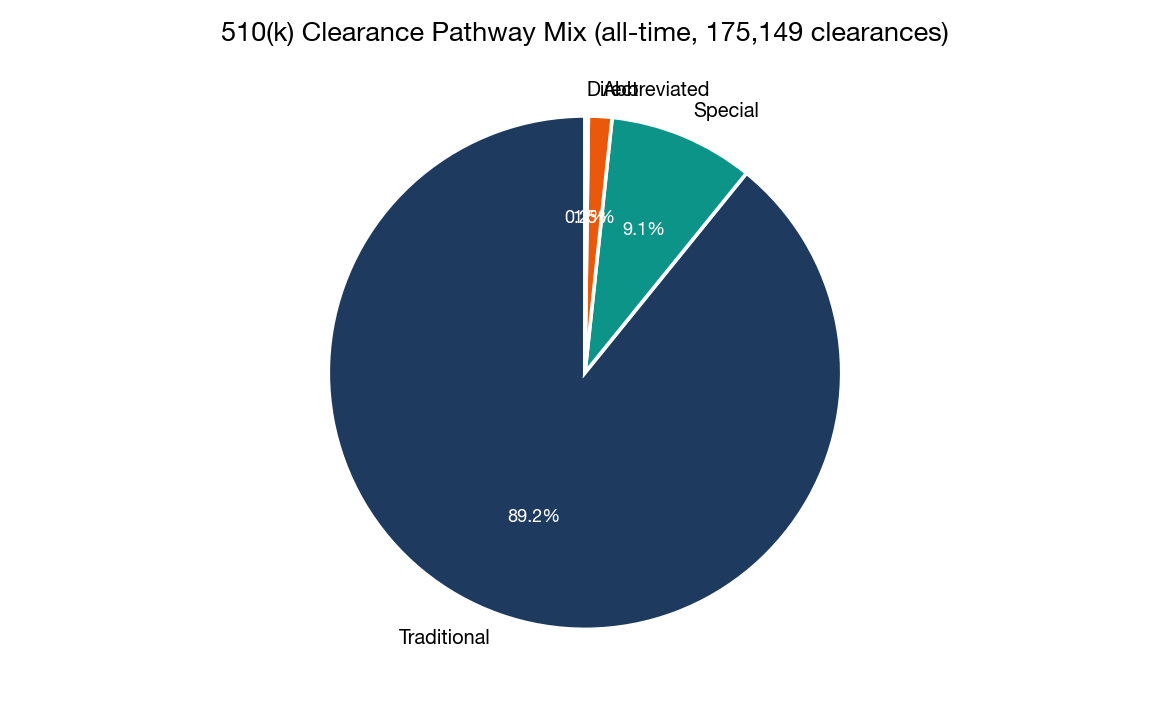

- Traditional 510(k) reviews grew from 80.6% of clearances in 2016 to 82.3% in 2025 — despite two decades of policy effort to shift work to the Special, Abbreviated, and Direct pathways, traditional review is not retreating

Regulatory Context: Advisory Committees and the 510(k) Pathway

Every 510(k) premarket notification is assigned to one of the FDA's device-area advisory committees (also called "review panels"), which correspond to medical specialties — Cardiovascular, Orthopedic, Radiology, Dental, and so on. The panel determines which FDA reviewers handle the submission, which product-code regulation applies, and, for higher-risk predicates, which clinical or performance data is expected. The advisory-committee field in the 510(k) database is therefore the closest available proxy for "what kind of device" at population scale.

Within each specialty, the FDA offers several 510(k) review tracks: Traditional (full review), Special (for devices modified in ways that can be reviewed against the manufacturer's own predicate with summary documentation), Abbreviated (for certain well-understood device types that can be reviewed against abbreviated data), and the rarer Direct pathway. Total annual 510(k) clearance volume has held remarkably steady at roughly 2,900–3,300 clearances per year for the last decade.

The growing Radiology share documented below is not happening in isolation. It tracks the surge in artificial-intelligence and machine-learning medical devices. The FDA authorized a record 295 AI/ML-enabled devices in 2025, and radiology accounted for roughly 75% of those AI/ML clearances — imaging computer-aided detection and diagnosis (product codes such as QIH, MYN, QKB) dominate the AI list (Innolitics, 2026; IntuitionLabs, 2026). That AI/ML concentration inside Radiology is a major reason the panel's overall share of 510(k) is climbing.

Data Source and Method

- Source: FDA 510(k) clearance database (full extract)

- Analysis sample: 175,149 510(k) clearance records

- Fields analyzed: Advisory committee (medical specialty), clearance type, decision date, applicant, product code

- Run date: 2026-06-14

- Method: All figures computed by MedDeviceGuide analysis of the full 510(k) extract. "Share by specialty" for a given year divides that specialty's clearances by all clearances finalized in the same year. Year-over-year comparisons use full years 2016 and 2025; 2026 figures are partial and excluded from trend calculations.

The All-Time Specialty Ranking

| Rank | Advisory Committee (Specialty) | Clearances | Share | Cumulative |

|---|---|---|---|---|

| 1 | Cardiovascular | 19,056 | 10.9% | 10.9% |

| 2 | Orthopedic | 16,957 | 9.7% | 20.6% |

| 3 | General, Plastic Surgery | 16,200 | 9.2% | 29.8% |

| 4 | General Hospital | 15,666 | 8.9% | 38.8% |

| 5 | Radiology | 14,546 | 8.3% | 47.1% |

| 6 | Clinical Chemistry | 13,041 | 7.4% | 54.5% |

| 7 | Dental | 12,598 | 7.2% | 61.7% |

| 8 | Gastroenterology, Urology | 11,247 | 6.4% | 68.1% |

| 9 | Anesthesiology | 8,386 | 4.8% | 72.9% |

| 10 | Microbiology | 6,918 | 3.9% | 76.9% |

| 11 | Neurology | 6,051 | 3.5% | 80.3% |

| 12 | Physical Medicine | 5,606 | 3.2% | 83.5% |

A handful of panels do most of the FDA's 510(k) work. Just eight specialties handle 68% of all clearances, which means review capacity, predicate depth, and reviewer expertise are concentrated in cardiovascular, orthopedic, surgical, general-hospital, radiology, IVD chemistry, dental, and gastro/urology devices. For manufacturers in these crowded panels, predicate selection and differentiation matter more than in the long tail; for manufacturers in smaller panels (Ophthalmic, Obstetrics/Gynecology, Hematology), reviewers see fewer comparable submissions and predicates can be thinner.

How the Specialty Mix Shifted (2016 vs 2025)

Comparing each specialty's share of annual clearances in 2016 versus 2025 shows which device fields are gaining and losing relative weight inside the FDA's review pipeline:

| Specialty | 2016 Share | 2025 Share | Change |

|---|---|---|---|

| Orthopedic | 16.0% | 12.6% | −3.4pp |

| Cardiovascular | 12.3% | 10.9% | −1.5pp |

| Clinical Chemistry | 3.1% | 1.7% | −1.5pp |

| General Hospital | 7.2% | 5.9% | −1.3pp |

| Dental | 7.8% | 7.1% | −0.7pp |

| Anesthesiology | 3.2% | 3.1% | −0.1pp |

| General, Plastic Surgery | 11.0% | 11.8% | +0.8pp |

| Microbiology | 2.1% | 3.8% | +1.7pp |

| Gastroenterology, Urology | 5.9% | 8.0% | +2.1pp |

| Radiology | 12.8% | 14.9% | +2.1pp |

Three patterns stand out:

Radiology is now the leading growth specialty (+2.1pp). This is the imaging-AI effect. Computer-aided triage, detection, and diagnosis software for X-ray, CT, and MRI dominates the FDA's AI/ML list, and each of those products enters through a 510(k) assigned to the Radiology panel. The 2025 AI/ML clearance record (295 devices, ~75% radiology) is visible in the panel's rising share.

Orthopedic is the biggest decliner (−3.4pp). Orthopedics is a mature hardware field with deep predicate chains; the declining share reflects saturation rather than contraction — the absolute number of orthopedic clearances remains high, but other fields are growing faster.

Diagnostics are gaining across the board. Microbiology (+1.7pp) and the Gastroenterology/Urology panel (+2.1pp, which captures many molecular and endoscopic devices) both rose, while Clinical Chemistry declined (−1.5pp) as traditional chemistry immunoassays consolidate. The net signal is a shift toward molecular, microbiology, and image-based diagnostics.

Clearance Pathway: Traditional Review Still Dominates

| Pathway | All-Time Clearances | Share |

|---|---|---|

| Traditional | 156,016 | 89.1% |

| Special | 15,995 | 9.1% |

| Abbreviated | 2,589 | 1.5% |

| Direct | 367 | 0.2% |

A common industry assumption is that alternative 510(k) pathways — Special, Abbreviated, and the Direct route — have gradually displaced traditional review. The data does not support that. Traditional 510(k) reviews actually grew from 80.6% of clearances in 2016 to 82.3% in 2025, while the Special 510(k) share edged down from 15.9% to 14.9% and Abbreviated halved from 2.5% to 1.3%.

The implication is that for the bulk of 510(k) submissions — including the growing volume of imaging-AI devices — full traditional review remains the default. Manufacturers should plan submission timelines against traditional-review expectations (median clearance in the range of 140–180 days for most panels) rather than assuming a faster pathway will apply.

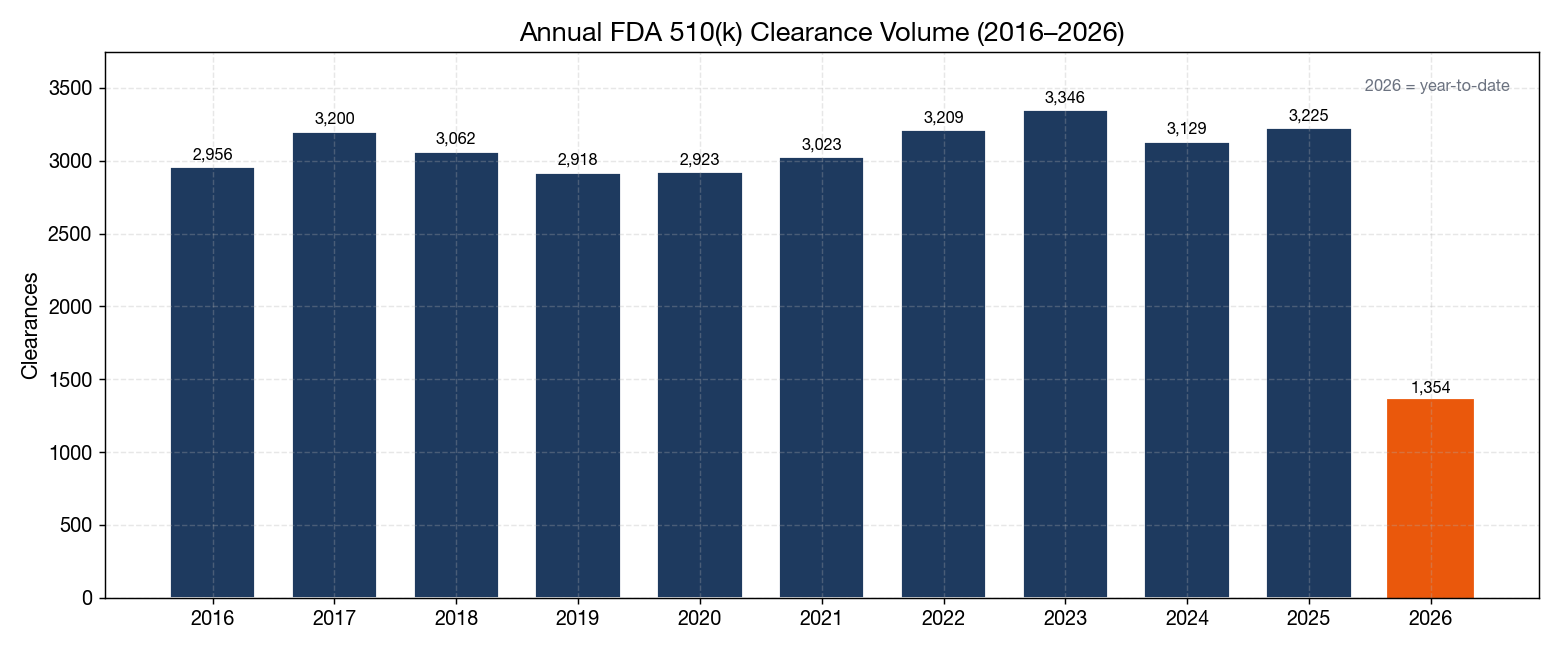

Annual Volume: A Steady Pipeline

| Year | Clearances |

|---|---|

| 2016 | 2,956 |

| 2017 | 3,200 |

| 2018 | 3,062 |

| 2019 | 2,918 |

| 2020 | 2,923 |

| 2021 | 3,023 |

| 2022 | 3,209 |

| 2023 | 3,346 |

| 2024 | 3,129 |

| 2025 | 3,225 |

| 2026 (YTD) | 1,354 |

Annual clearance volume has stayed within a narrow ~2,900–3,350 band for a decade. The notable story is not the total — it is the changing composition inside that steady total: more radiology and diagnostic software, fewer orthopedic hardware variants. FDA's review capacity is roughly fixed, so the specialty-mix shift means reviewers in growing panels (Radiology, Microbiology) are seeing rising caseloads while orthopedic and general-hospital reviewers see relatively less.

Practical Implications

1. Predicate Selection Is Hardest in the Top Panels

In Cardiovascular, Orthopedic, Plastic Surgery, General Hospital, and Radiology — the panels that together handle nearly half of all clearances — the predicate universe is deep, which is both an advantage and a trap. A well-chosen predicate accelerates review; a poorly chosen one (different technology, different intended use, or a predicate with its own unresolved issues) is the most common cause of AI (Additional Information) hold. Invest in predicate analysis before drafting.

2. Radiology and AI: Expect a Crowded, Fast-Moving Panel

Radiology is now the highest-momentum panel. Manufacturers of imaging devices — especially AI/ML triage, detection, and diagnosis software — are entering a panel where 75% of AI/ML clearances already sit. Differentiation increasingly depends on clinical-performance evidence, bias evaluation across patient populations, and a Predetermined Change Control Plan (PCCP) for model updates, rather than on raw predicate similarity.

3. Diagnostics Manufacturers Should Watch Microbiology

The +1.7pp gain in Microbiology and the +2.1pp gain in Gastroenterology/Urology point to growing review activity in molecular and microbiology diagnostics. Manufacturers in infectious-disease molecular assays, antimicrobial susceptibility, and GI testing face a panel that is becoming busier but where predicates can still be thinner than in clinical chemistry — an opportunity for well-substantiated submissions.

4. Orthopedic and Cardiovascular: Plan for Predicate Saturation

The declining share in Orthopedic and Cardiovascular does not mean these panels are shrinking in absolute terms — it means the predicate chains are mature and reviewers expect more differentiation. New orthopedic or cardiovascular 510(k)s need strong bench and sometimes clinical data to distinguish themselves from an extensive predicate field; "me-too" submissions face heightened scrutiny.

5. Plan Submission Timelines Against Traditional Review

Because Traditional review covers 82% of clearances and its share is rising, default planning should assume full review (roughly 5–6 months from acceptance to decision for most panels, longer for complex submissions). The Special 510(k) and Direct pathways remain useful but narrow tools — do not build launch timelines assuming they will apply.

6. Use the Panel to Anticipate Reviewer Expertise

The advisory committee a device lands in determines the reviewers and the regulatory-statute citations. Manufacturers can use the all-time specialty distribution to gauge how many comparable predicates exist for a given panel and how busy those reviewers are. Smaller panels (Ophthalmic, OB/GYN, Hematology) mean fewer reviewers and fewer predicates — submissions there may take longer to find the right reviewer but face less crowded competition once cleared.

Data Source and Method Notes

- Primary data: FDA 510(k) clearance database, full extract dated 2026-06-10, 175,149 records.

- Analysis: MedDeviceGuide analysis of the full 510(k) extract. All figures computed directly from the dataset.

- Advisory committee: The FDA's "advisory committee" field on each 510(k) record, which corresponds to the device review panel and medical specialty. A small number of records (4,652, 2.7%) carry "Unknown" or blank committee values; these are excluded from share calculations.

- Year-over-year comparison: Full years 2016 and 2025 are used for the mix-shift analysis; 2026 is excluded as a partial year. Shares are computed within each calendar year.

- Clearance-type trend: Based on the FDA's clearance-type field (Traditional, Special, Abbreviated, Direct, plus minor Post-NSE and Dual Track categories).

- Limitations: Advisory-committee assignment reflects the panel a submission is routed to and is a strong but imperfect proxy for clinical specialty (some cross-cutting devices are assigned to the most fitting panel). AI/ML clearance figures cited for context come from the FDA's separately maintained AI/ML-Enabled Medical Devices list and the Innolitics year-in-review, not from the advisory-committee field alone.

Data source: FDA 510(k) clearance database (full extract, dated 2026-06-10). Analysis by MedDeviceGuide, run date 2026-06-14. AI/ML context from Innolitics (2026) and IntuitionLabs (2026), drawn from the FDA's AI/ML-Enabled Medical Devices list.