Canada MDALL Class III/IV Analysis: US Companies Hold 48% of High-Risk Listings

US companies hold 48% of Canada's 57,000 Class III/IV MDALL listings. Median device age is 9.7 years and 49% of devices are over a decade old. Full data analysis.

Executive Summary

Health Canada's Medical Devices Active Licence Listing (MDALL) is the definitive public record of all licensed Class II, III, and IV medical devices authorized for sale in Canada. Our analysis of the complete MDALL active device dataset (enriched extract, 5 June 2026) reveals a market dominated by US-headquartered companies, with an aging device portfolio and significant concentration among a small number of large orthopaedic and cardiovascular firms.

Key findings from the analysis of 152,560 active device listings:

- United States companies hold 47.9% of all Class III/IV listings (27,467 of 57,335)

- North American companies collectively control 50.5% of Class III/IV; European companies hold 32.0%

- Medtronic leads Class IV (highest risk) with 910 listings, followed by Boston Scientific (724 combined)

- 48.8% of all active MDALL listings are over 10 years old, with a median device age of 9.7 years

- The top 10 companies control 20.4% of all Class III/IV listings

Data Source and Method

- Source: Health Canada Medical Devices Active Licence Listing (MDALL), enriched extract

- Analysis sample: Health Canada MDALL active-device extract dated 5 June 2026 (152,561 rows)

- Scope: All active device entries with risk class, company information, country code, and licence dates

- Analysis date: 6 June 2026

- Computed using: MedDeviceGuide analysis of the MDALL public extract

MDALL is updated daily by Health Canada and contains product-specific information on all currently licensed Class II, III, and IV medical devices. Class I devices are not included (they require a Medical Device Establishment Licence, or MDEL, rather than individual device licences).

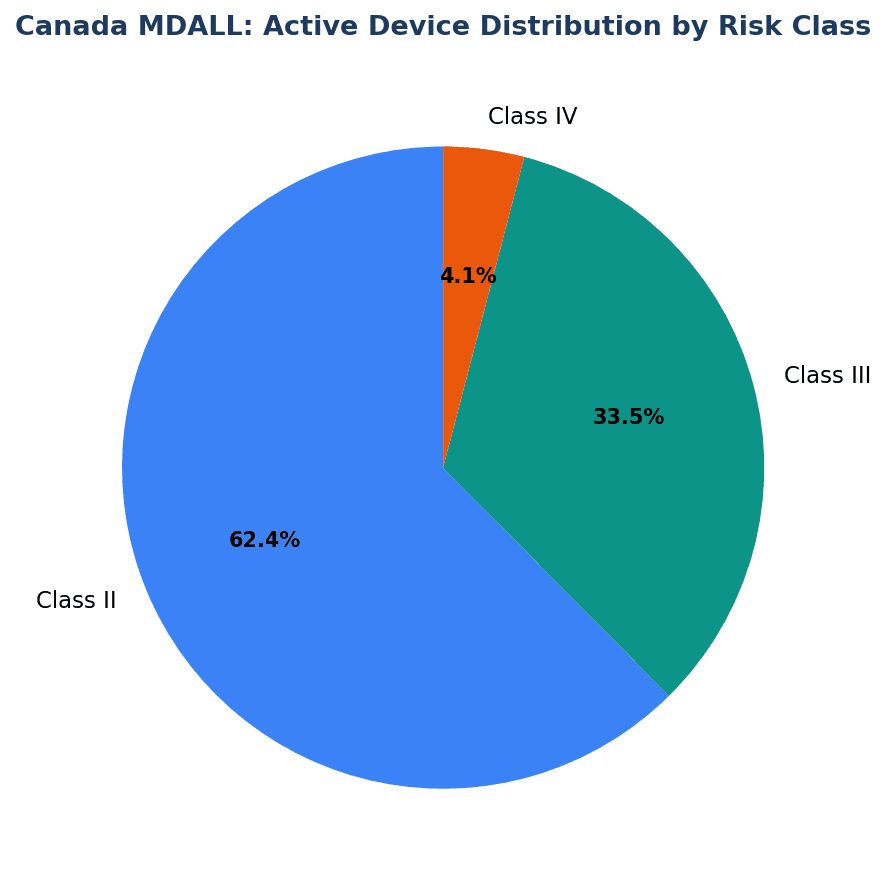

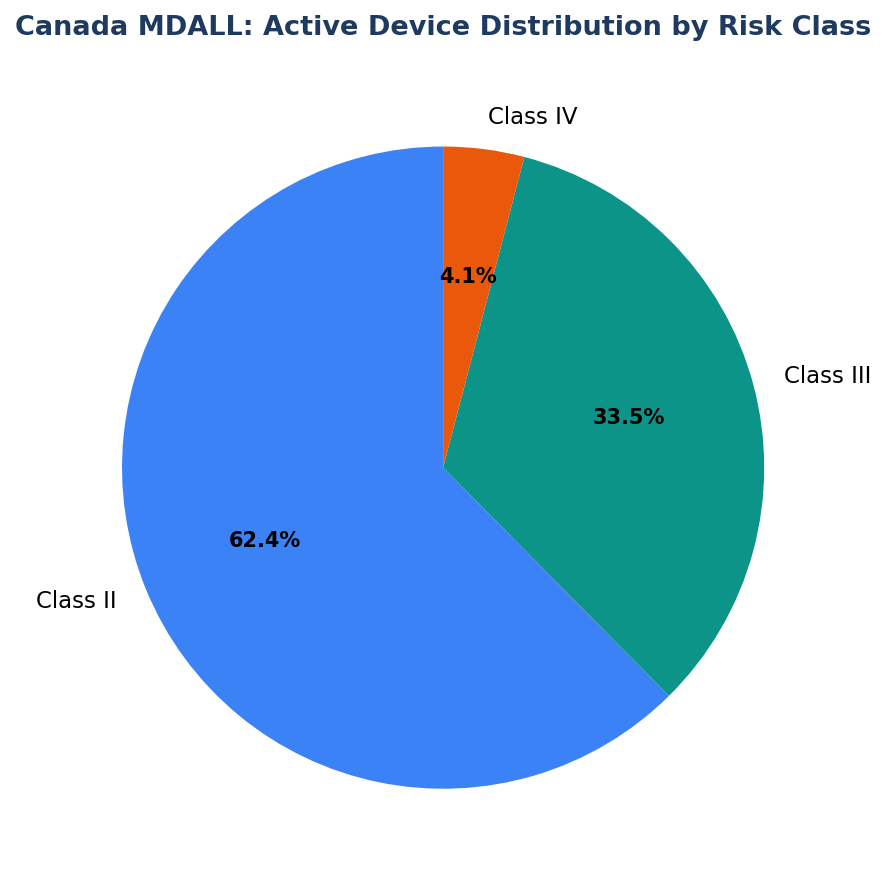

Risk Class Distribution

| Risk Class | Listings | Share |

|---|---|---|

| Class II | 95,225 | 62.4% |

| Class III | 51,128 | 33.5% |

| Class IV | 6,207 | 4.1% |

| Total | 152,560 | 100% |

Class II devices (moderate risk, such as powered wheelchairs, surgical gloves, and some infusion pumps) account for nearly two-thirds of all active listings. Class III (higher risk — implants, diagnostic imaging) and Class IV (highest risk — pacemakers, heart valves, implantable defibrillators) together represent 37.6% of the database.

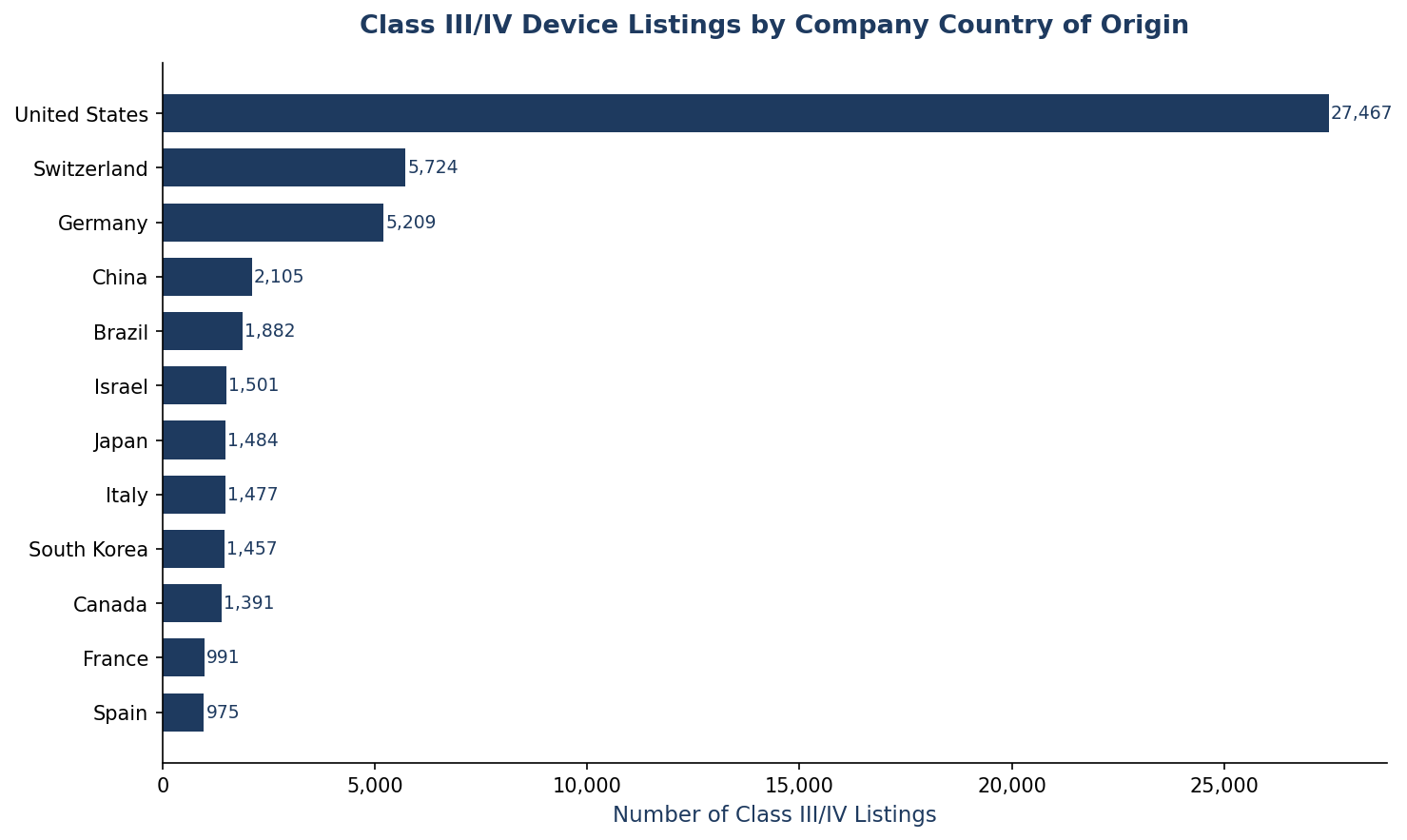

Country of Origin: Class III/IV

| Rank | Country | Class III/IV Listings | Share |

|---|---|---|---|

| 1 | United States | 27,467 | 47.9% |

| 2 | Switzerland | 5,724 | 10.0% |

| 3 | Germany | 5,209 | 9.1% |

| 4 | China | 2,105 | 3.7% |

| 5 | Brazil | 1,882 | 3.3% |

| 6 | Israel | 1,501 | 2.6% |

| 7 | Japan | 1,484 | 2.6% |

| 8 | Italy | 1,477 | 2.6% |

| 9 | South Korea | 1,457 | 2.5% |

| 10 | Canada | 1,391 | 2.4% |

| 11 | France | 991 | 1.7% |

| 12 | Spain | 975 | 1.7% |

Note: The "country" field in MDALL refers to the company (licence holder) address, not necessarily where the device is physically manufactured. A US company listing a device manufactured in Mexico would still appear under "US."

Several observations:

- Switzerland's outsized presence (10.0%) is driven by companies like Synthes GmbH (DePuy Synthes/J&J) and Stryker GmbH, which hold European corporate registrations but serve global markets.

- Brazil's #5 position (1,882 listings) is largely attributable to JJGC Indústria e Comércio de Materiais Dentários (1,688 listings), a major dental device manufacturer.

- China's 2,105 listings reflect the growing number of Chinese device manufacturers obtaining Canadian market access, led by Shenzhen Mindray (1,413 listings).

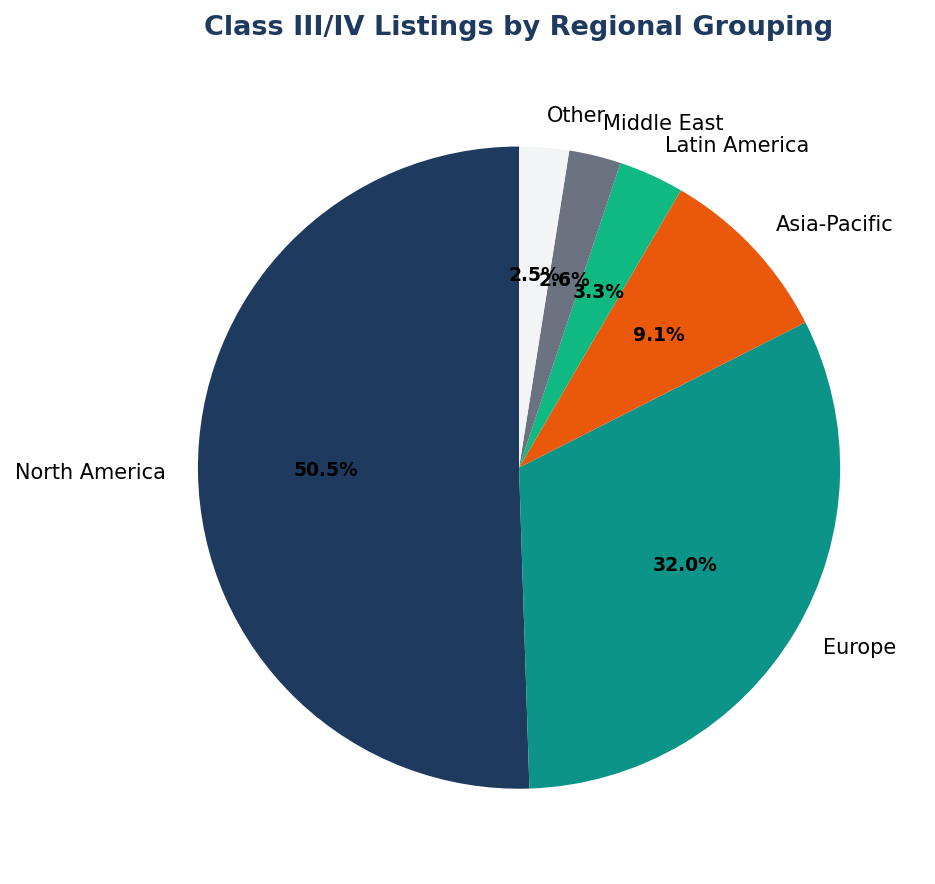

Regional Grouping: Class III/IV

| Region | Listings | Share |

|---|---|---|

| North America (US, CA, MX) | 28,963 | 50.5% |

| Europe (16 countries) | 18,322 | 32.0% |

| Asia-Pacific (6 countries) | 5,229 | 9.1% |

| Latin America (BR, AR, CO) | 1,886 | 3.3% |

| Middle East (Israel) | 1,501 | 2.6% |

| Other | 1,434 | 2.5% |

North American and European companies together account for 82.5% of all Class III/IV listings. Asia-Pacific — despite being the fastest-growing region for medical device manufacturing — holds less than 10% of Canadian high-risk device licences.

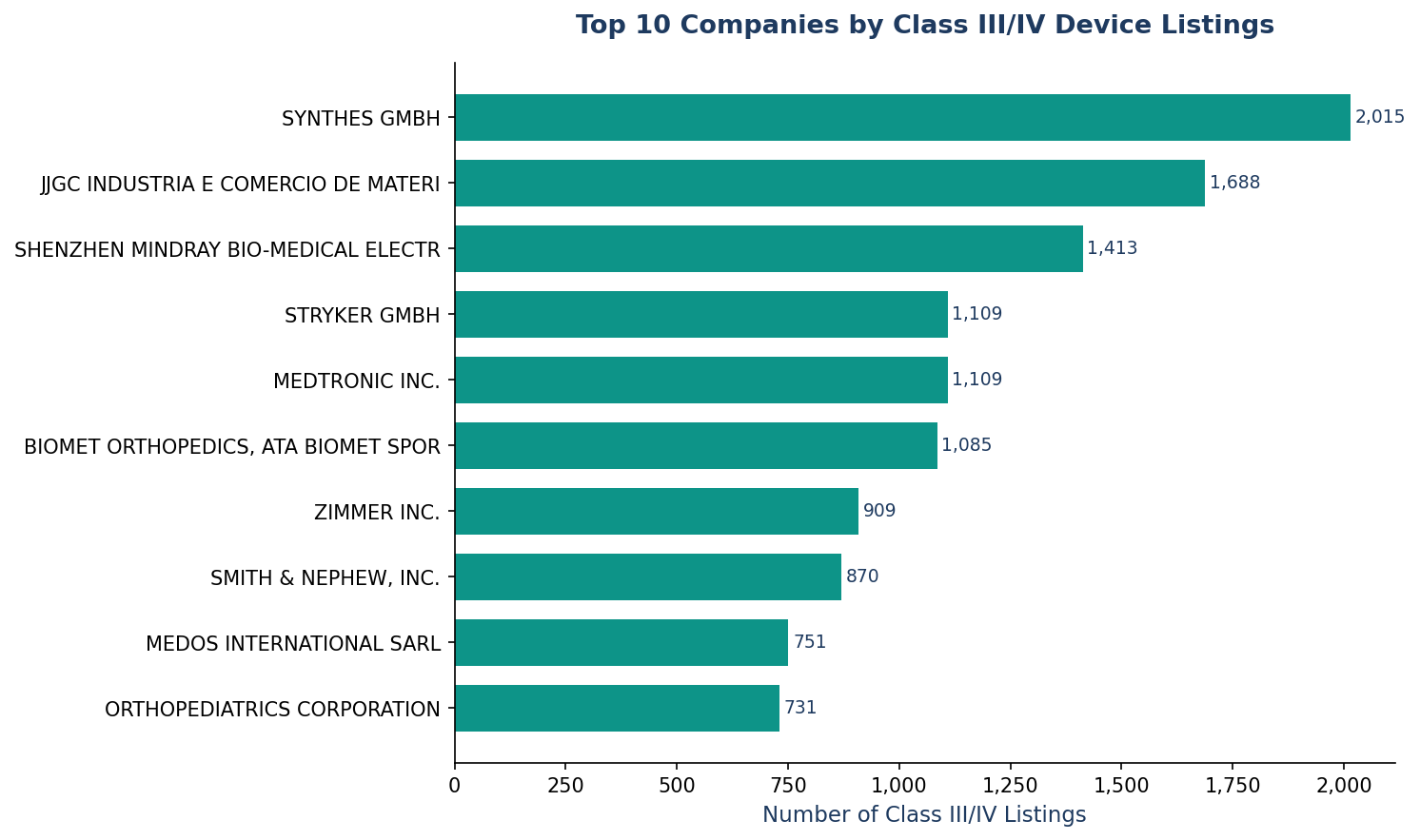

Company Concentration

| Rank | Company | Class III/IV Listings |

|---|---|---|

| 1 | Synthes GmbH (J&J) | 2,015 |

| 2 | JJGC (Brazil, dental) | 1,688 |

| 3 | Shenzhen Mindray | 1,413 |

| 4 | Stryker GmbH | 1,109 |

| 5 | Medtronic Inc. | 1,109 |

| 6 | Biomet (Zimmer Biomet) | 1,085 |

| 7 | Zimmer Inc. | 909 |

| 8 | Smith & Nephew, Inc. | 870 |

| 9 | Medos International SARL | 751 |

| 10 | OrthoPediatrics Corp. | 731 |

The orthopaedic sector dominates the concentration picture. Synthes (DePuy Synthes), Stryker, Biomet, Zimmer, Smith & Nephew, and OrthoPediatrics collectively hold over 6,700 Class III/IV listings — nearly 12% of all high-risk entries. This reflects the inherently high-risk classification of orthopaedic implants and the broad product portfolios of these manufacturers.

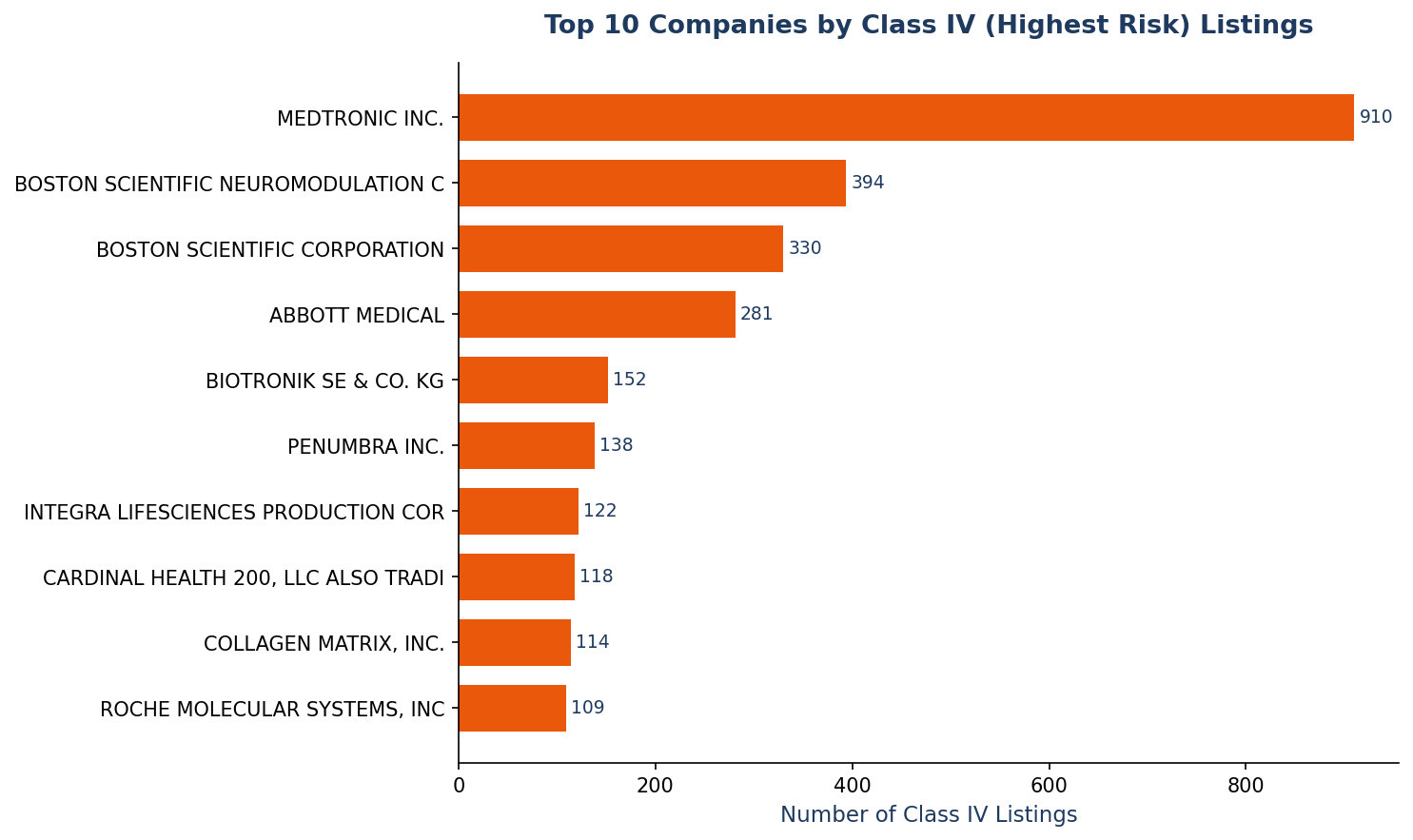

Class IV: The Highest-Risk Category

Class IV devices — the highest-risk category, including implantable defibrillators, heart valves, and neurostimulators — contain 6,207 active listings. The company profile is even more concentrated than Class III:

| Rank | Company | Class IV Listings | Country |

|---|---|---|---|

| 1 | Medtronic Inc. | 910 | US |

| 2 | Boston Scientific Neuromodulation | 394 | US |

| 3 | Boston Scientific Corporation | 330 | US |

| 4 | Abbott Medical | 281 | US |

| 5 | Biotronik SE & Co. KG | 152 | DE |

| 6 | Penumbra Inc. | 138 | US |

| 7 | Integra LifeSciences | 122 | US |

| 8 | Cardinal Health | 118 | US |

| 9 | Collagen Matrix, Inc. | 114 | US |

| 10 | Roche Molecular Systems | 109 | US |

Nine of the top 10 Class IV companies are US-headquartered. Only Biotronik (Germany) breaks the US dominance in the highest-risk tier. This concentration reflects the US medtech industry's dominance in implantable and life-sustaining device categories.

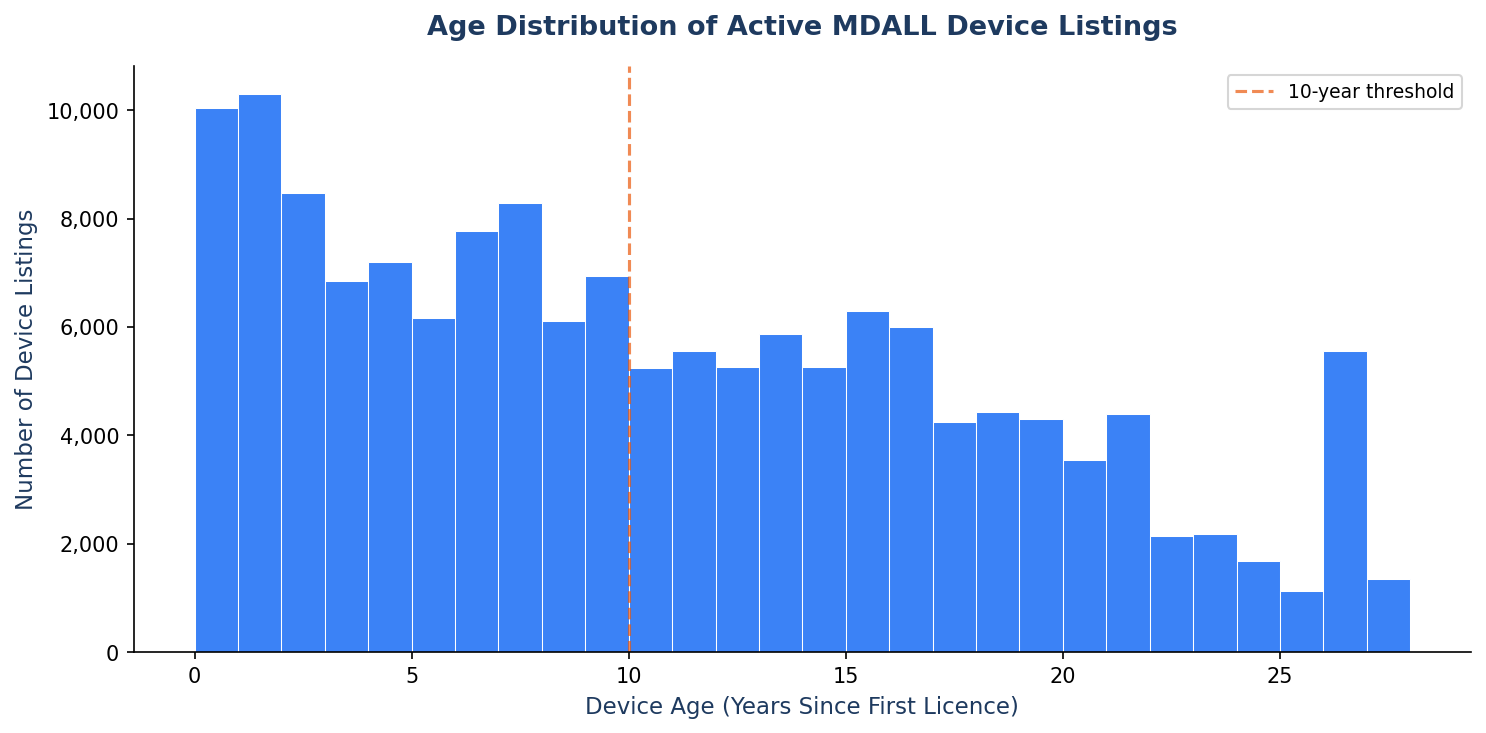

Device Age: An Aging Portfolio

| Age Bucket | Listings | Share |

|---|---|---|

| < 2 years | 20,347 | 13.3% |

| 2–5 years | 22,518 | 14.8% |

| 5–10 years | 35,256 | 23.1% |

| 10+ years | 74,439 | 48.8% |

Nearly half of all active MDALL listings are over 10 years old. The median device age is 9.7 years; the mean is 10.9 years. This has several implications:

Legacy device dominance: Many Class III/IV devices on the Canadian market were first licensed a decade or more ago. These legacy devices may have been submitted under older regulatory standards that differ from current Health Canada expectations.

Post-market surveillance burden: Older devices accumulate longer post-market histories, which can be an asset for safety monitoring — but may also mean that device labelling, cybersecurity features, and clinical evidence no longer meet current best practices.

Opportunity for new entrants: The aging portfolio creates market entry opportunities for manufacturers with newer devices that incorporate updated technology, improved clinical evidence, and stronger cybersecurity controls — particularly in areas where Health Canada's 2026 guidance updates emphasize lifecycle-based regulation.

Licence Types and Status

Class III/IV listings break down by licence type as follows:

| Licence Type | Class III/IV Listings |

|---|---|

| System | 38,296 (66.8%) |

| Device Family | 11,234 (19.6%) |

| Device Group Family | 4,887 (8.5%) |

| Test Kit | 1,434 (2.5%) |

| Single Device | 1,184 (2.1%) |

| Device Group | 300 (0.5%) |

"System" licences dominate, reflecting the common practice of registering multiple compatible devices under a single system entry (e.g., an imaging system with its accessories). The 2.5% share of "Test Kit" entries reflects IVD devices in the Class III/IV range.

Practical Implications

For Manufacturers Entering Canada

US dominance means US precedent: With US companies holding nearly half of all Class III/IV listings, Health Canada reviewers are deeply familiar with FDA submissions, 510(k) clearance letters, and US clinical data. Manufacturers with FDA clearance already have a significant procedural advantage.

MDL vs. MDEL pathway clarity: Class II devices (62.4% of MDALL) require a Medical Device Licence (MDL) application, but the review is typically less intensive than Class III/IV. New entrants should consider starting with Class II products to build familiarity with Health Canada's submission process.

Age of existing licences: If you are introducing a device that competes with a 10+ year-old licensed product, you may have an advantage in clinical evidence, cybersecurity documentation, and real-world data — especially under Health Canada's 2026 guidance updates that strengthen lifecycle assessment.

For Market Intelligence Teams

- The top 10 Class III/IV companies are known entities. Competitor analysis should focus on which of their specific System and Device Family entries are due for renewal or significant change, rather than raw listing counts.

- Chinese manufacturers (led by Mindray with 1,413 listings) are the fastest-growing segment in Canadian device licensing. Monitor NMPA-to-Health Canada pathway filings.

- Brazilian dental device registrations (JJGC: 1,688 listings) represent an unusually concentrated niche that may face increased regulatory scrutiny.

Method Notes

- All figures are computed from the enriched MDALL extract dated 5 June 2026.

- "Company country" is the country code associated with the licence holder's address in MDALL, not the country of physical manufacture.

- Device age is calculated from the

device_first_licence_dtfield to the analysis date (5 June 2026). - Licence status "I" = Active; "D" = Discontinued. Only active licences are included.

Sources

- Health Canada Medical Devices Active Licence Listing (MDALL). Updated daily. Accessed via enriched extract, 5 June 2026.

- Health Canada Medical Devices Directorate Performance Annual Report, April 2024 – March 2025 (published 30 May 2025).

- Health Canada guidance documents published March–April 2026: terms and conditions for Class II–IV devices, clinical evidence across the lifecycle, AI/ML-enabled devices.

- MedDeviceGuide analysis of the MDALL public extract, run date 6 June 2026.