Bahrain NHRA: 3 ARs Hold 55% of Devices — Small GCC Market Channel Lock-In

Bahrain NHRA device database analysis: 62 ARs manage 1,491 devices, top 3 hold 55%, all tracked licenses expired, and manufacturer-AR lock-in is high. GCC channel strategy implications.

Executive Summary

Bahrain's National Health Regulatory Authority (NHRA) requires every foreign medical device manufacturer to appoint an Authorized Representative (AR) — a local entity registered with NHRA that manages regulatory submissions, importation, and post-market compliance. With mandatory device registration enforced from 1 February 2026, the AR landscape is the single most important channel decision for market entry.

Our analysis of the NHRA device database (extracted 5 June 2026, 1,491 device listings) and the AR registry (142 registered ARs) reveals a market with striking concentration: just 3 ARs control 54.9% of all registered devices, while the AR registry lists 142 companies — meaning the vast majority of registered ARs hold zero or minimal device listings. The device data also shows that all tracked licenses have expiry dates before 2026, suggesting the dataset captures the pre-mandatory-registration baseline rather than the current active register.

This article quantifies the AR concentration, maps the channel lock-in dynamics, and explains why small GCC markets like Bahrain create unique switching costs that manufacturers should understand before committing to an AR.

Data Source and Method

- Source: Bahrain NHRA public device register and AR registry

- Analysis samples:

- Bahrain NHRA registered-device extract dated 5 June 2026 (1,491 device rows)

- Bahrain NHRA authorized-representative extract dated 5 June 2026 (142 AR rows)

- Analysis date: 6 June 2026

- Computed using: MedDeviceGuide analysis of NHRA public extracts

- Limitations: The device dataset appears to be a single extract from August 2023 source PDFs. All license expiry dates pre-date the analysis date, indicating these represent the historical register prior to the mandatory registration deadline. The AR registry is more current. Concentration patterns are representative of the market structure but may not reflect post-mandatory-registration changes.

NHRA Regulatory Context

Bahrain's NHRA operates under Resolution No. 48 of 2020 and the Medical Devices Regulation framework. Key points:

- Mandatory registration enforced from 1 February 2026

- Four-class system aligned with EU standards (Class I low risk, Class IIa/IIb moderate, Class III high risk)

- AR requirement: Only ARs registered with NHRA can submit device registrations

- Registration process: Through NHRA's Ajheza system; standard review is 40-80 working days (8-16 weeks), fast-track (via third-party services) is 20-40 working days

- License validity: 1 year, with renewal required at most 1 month before expiry

- UDI/traceability: NHRA introduced UDI-based traceability requirements with enforcement from July 2026

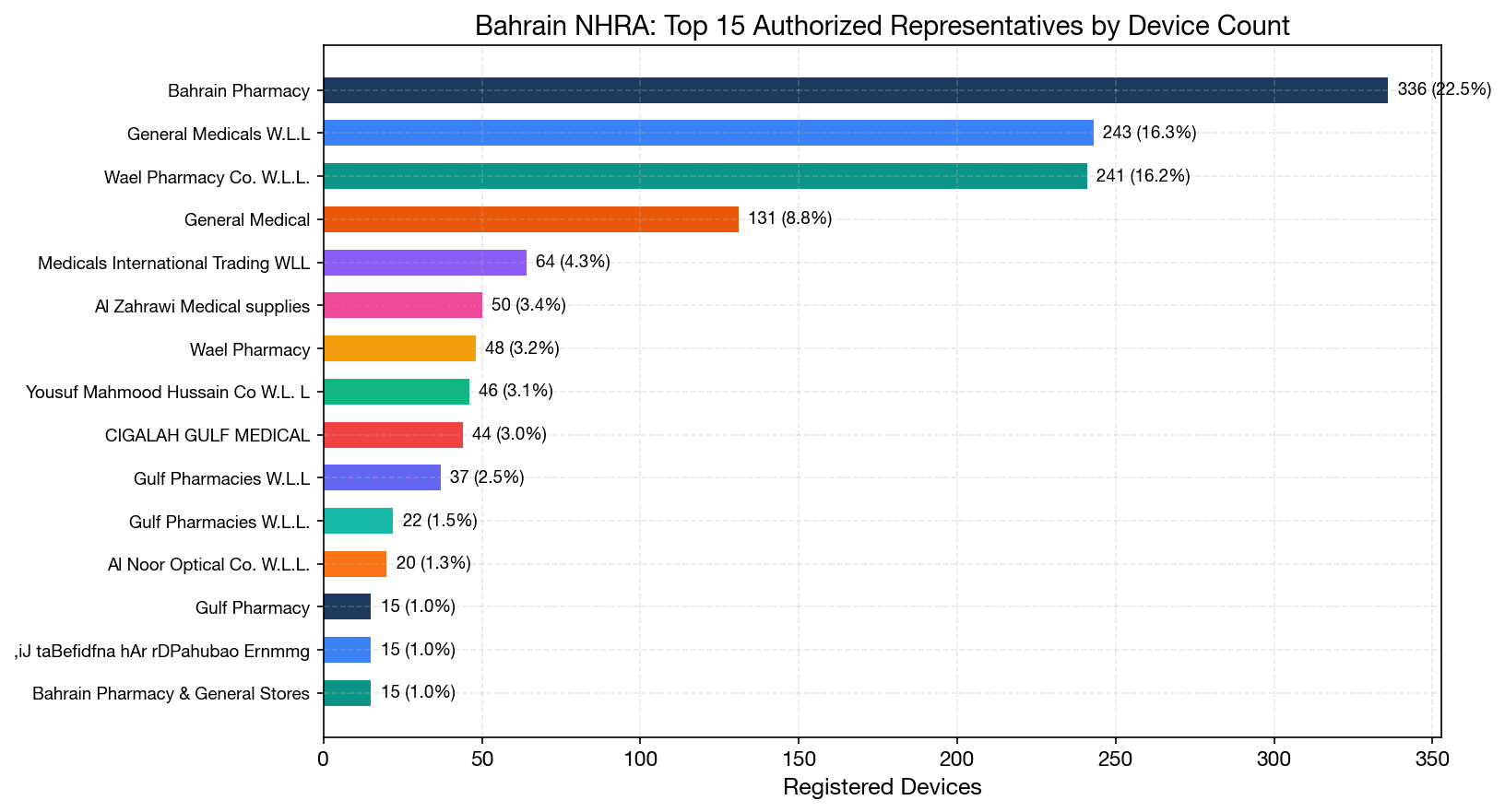

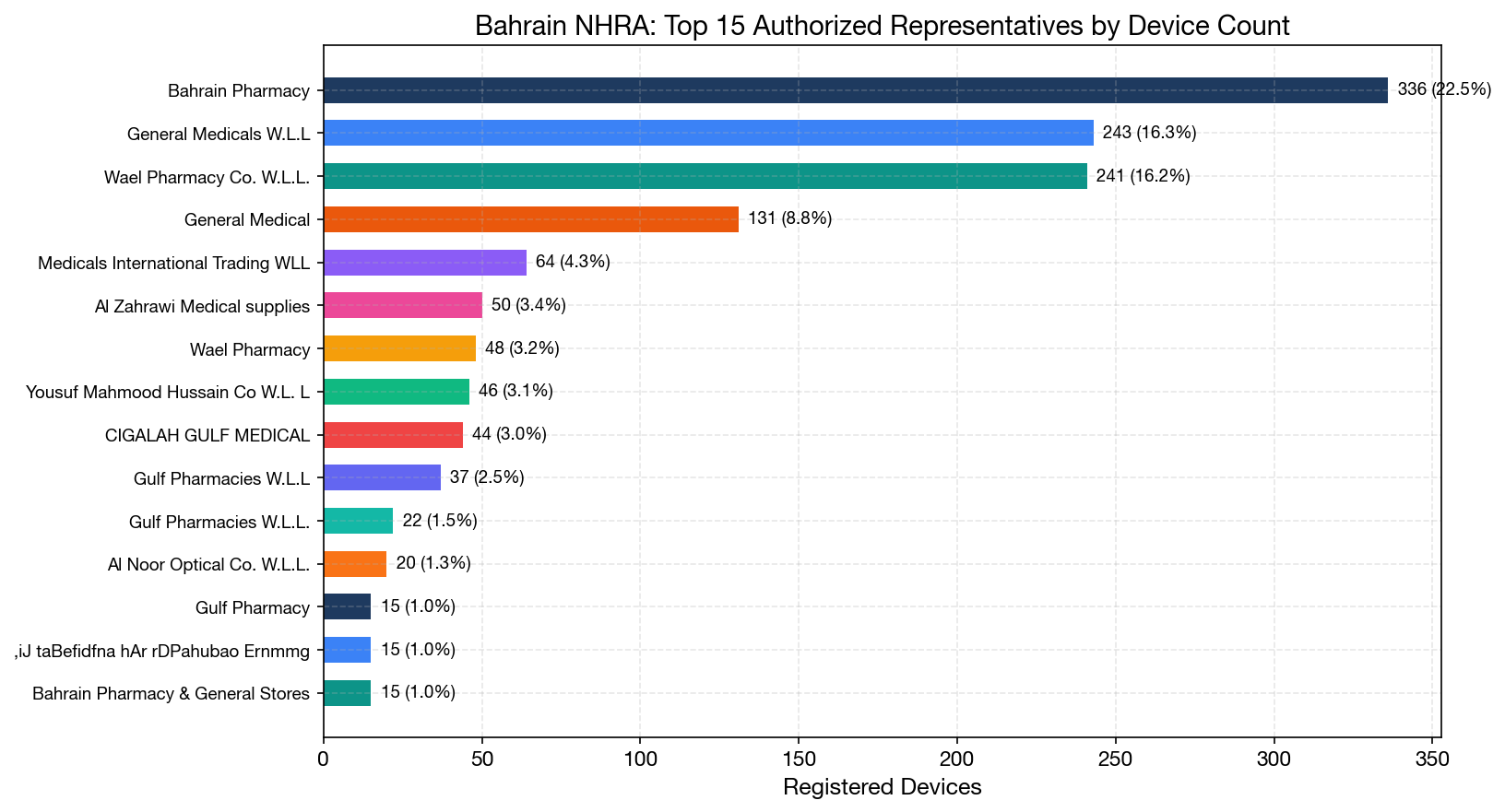

Authorized Representative Concentration

The device database lists 62 unique ARs managing 1,491 devices. The concentration is extreme:

Top 15 ARs by Device Count

| Authorized Representative | Devices | Share |

|---|---|---|

| Bahrain Pharmacy | 336 | 22.5% |

| General Medicals W.L.L | 243 | 16.3% |

| Wael Pharmacy Co. W.L.L. | 241 | 16.2% |

| General Medical | 71 | 4.8% |

| Medicals International Trading | 64 | 4.3% |

| General Medical (variant) | 60 | 4.0% |

| Al Zahrawi Medical Supplies | 50 | 3.4% |

| Yousuf Mahmood Hussain Co. | 46 | 3.1% |

| Cigalah Gulf Medical | 43 | 2.9% |

| Gulf Pharmacies W.L.L | 37 | 2.5% |

Concentration Metrics

| Metric | Value |

|---|---|

| Top 3 ARs | 820 devices (54.9%) |

| Top 5 ARs | 955 devices (64.1%) |

| Top 10 ARs | 1,191 devices (79.9%) |

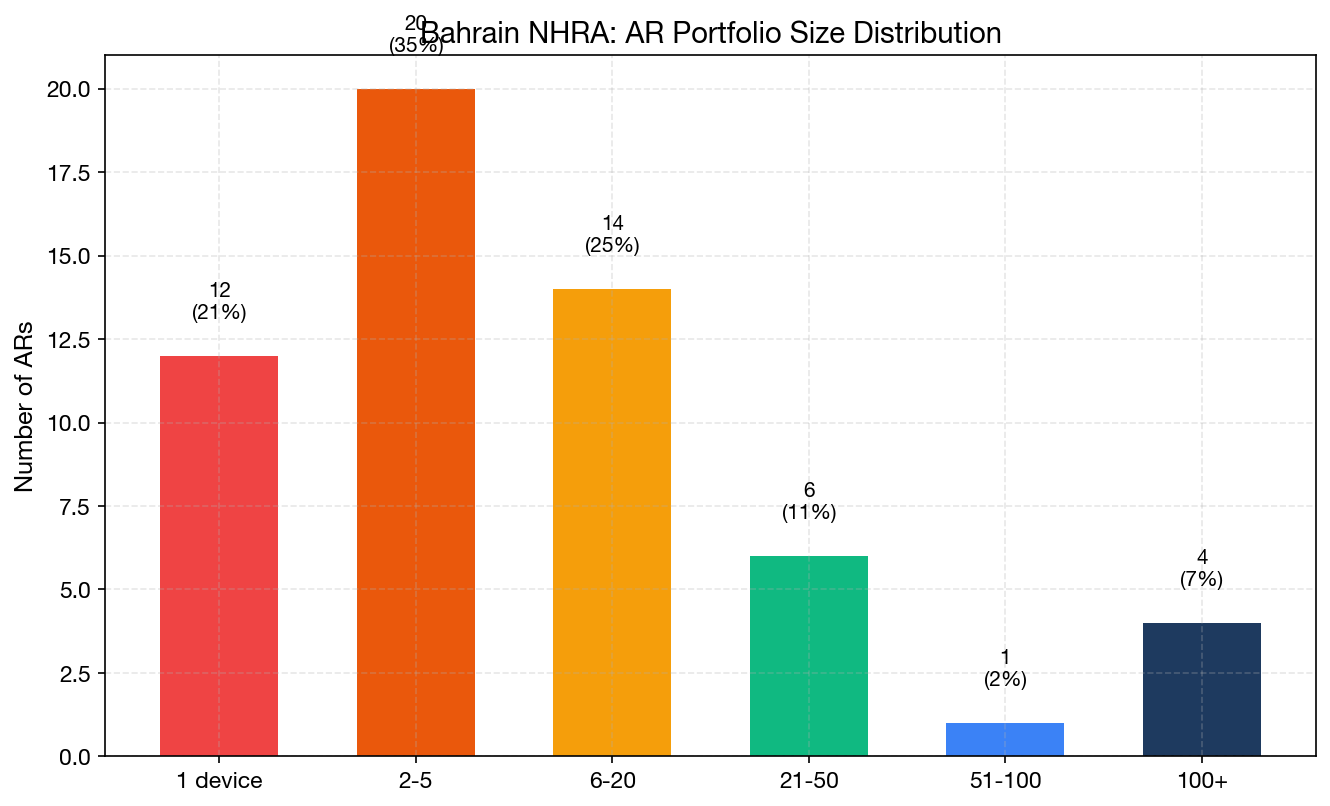

| Single-device ARs | 15 (24.2% of active ARs) |

Bahrain Pharmacy alone holds 22.5% of all device registrations — a level of single-entity dominance that is unusual even in small markets. Combined with General Medicals W.L.L and Wael Pharmacy, these three entities control more than half the market.

Note: The data contains naming variations (e.g., "General Medicals W.L.L", "general Medical", "General Medical") that likely represent the same entity. If consolidated, concentration would be even higher.

AR Portfolio Distribution

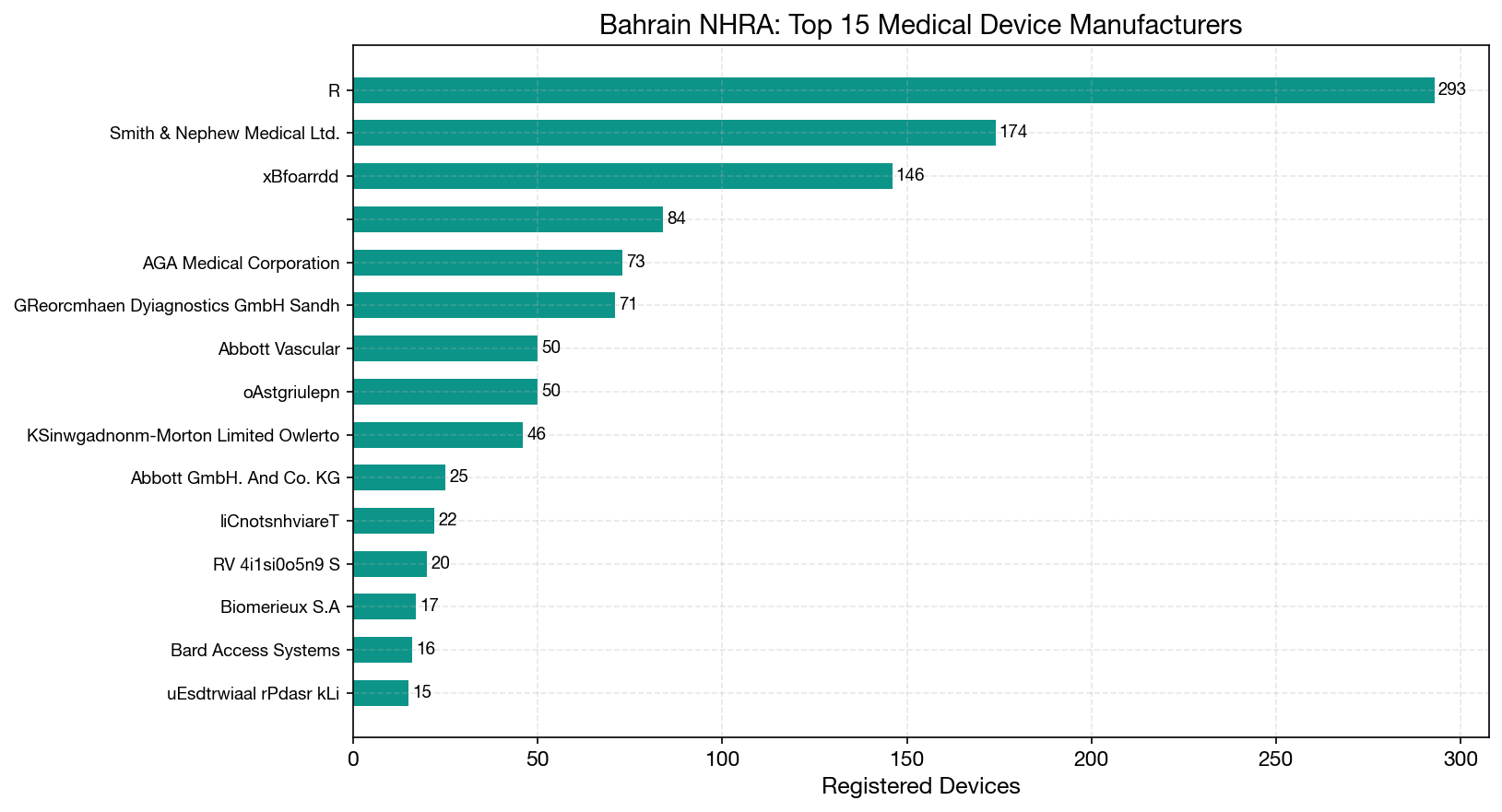

Manufacturer Landscape

The device database reveals 148 unique manufacturers (legal or physical), led by:

| Manufacturer | Devices |

|---|---|

| Roche Diagnostics GmbH (Germany) | ~314 |

| Smith & Nephew Medical Ltd (UK) | 163 |

| Bard Peripheral Vascular (USA) | 146 |

| AGA Medical Corporation (USA) | 73 |

| Abbott Vascular (USA) | 50 |

| CooperVision Manufacturing | 64 |

| Swann-Morton Limited (UK) | 46 |

| Abbott GmbH (Germany) | 25 |

| Biomerieux S.A (France) | 17 |

The manufacturer list is dominated by large multinational device companies, consistent with Bahrain's market structure: high-value specialty devices (vascular, wound care, ophthalmology, diagnostics) imported through a small number of local representatives.

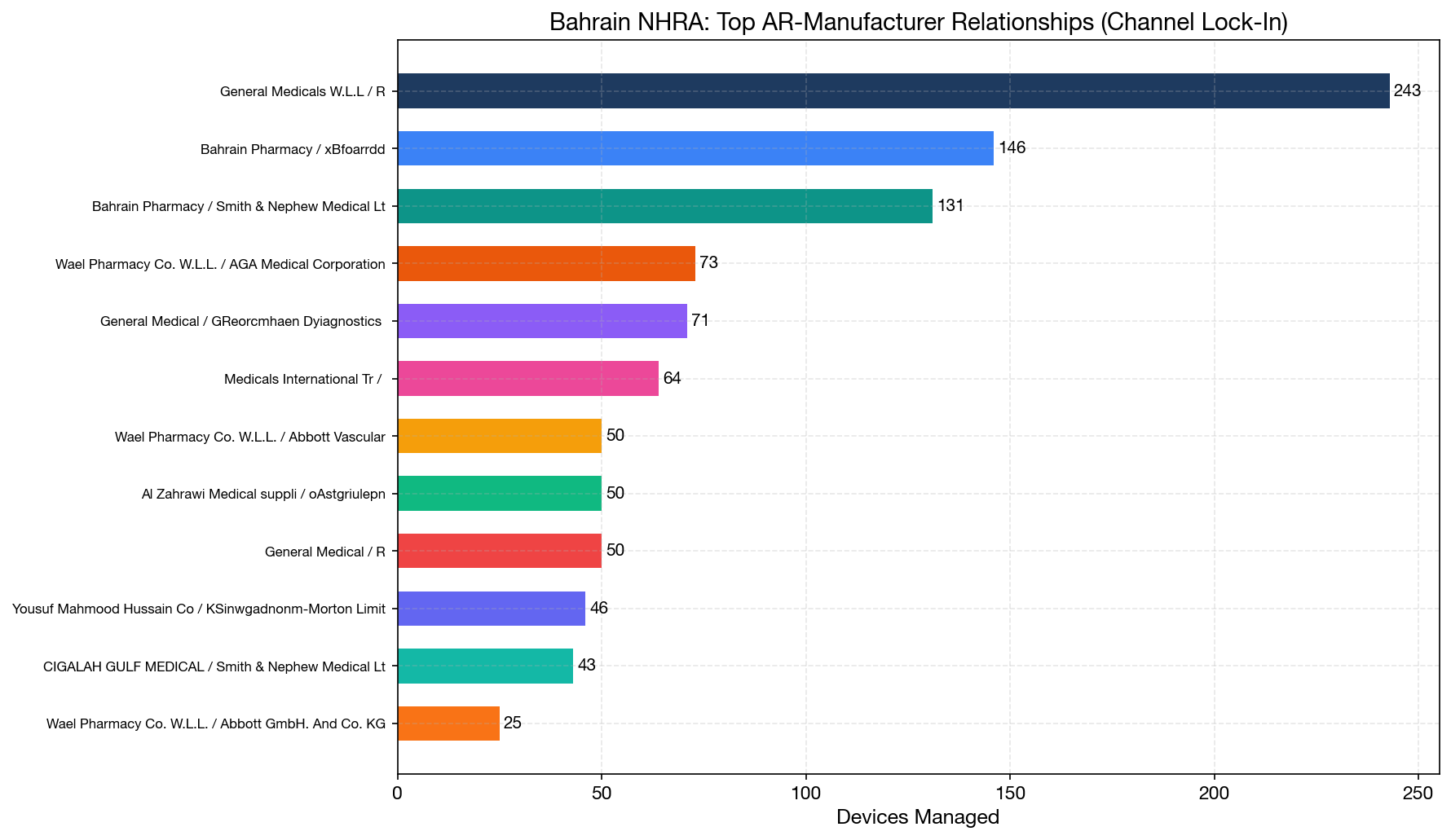

Channel Lock-In: AR-Manufacturer Relationships

Small markets create natural lock-in. When a manufacturer registers devices through an AR, switching ARs requires re-registration or transfer of all device licenses — a process that in Bahrain requires NHRA notification and documentation updates for each device individually.

Top AR-Manufacturer Relationships

| AR | Manufacturer | Devices |

|---|---|---|

| General Medicals W.L.L | Roche Diagnostics | ~263 |

| Bahrain Pharmacy | Bard Peripheral Vascular | 146 |

| Bahrain Pharmacy | Smith & Nephew | 120 |

| Wael Pharmacy Co. | AGA Medical (Abbott) | 73 |

| General Medical | Roche Diagnostics | ~121 |

| Medicals International | CooperVision | 64 |

| Wael Pharmacy Co. | Abbott Vascular | 50 |

| Al Zahrawi Medical | Coloplast/Agiliti | 50 |

The Roche Diagnostics-General Medicals relationship (~263 devices) is the single largest AR-manufacturer pairing in Bahrain. Similarly, Bahrain Pharmacy's combined Bard and Smith & Nephew portfolio (266 devices) represents deep channel integration.

Why This Matters

- Switching costs are proportional to portfolio size. A manufacturer with 100+ devices through one AR faces significant regulatory workload to transfer to a new AR.

- Post-market obligations travel with the AR. Field safety notices, adverse event reporting, and complaint handling all flow through the AR. Switching mid-cycle risks compliance gaps.

- NHRA license validity is only 1 year, with renewal due at most 1 month before expiry. This short validity period means manufacturers must maintain an active renewal cadence, and AR switching must be timed within the validity window.

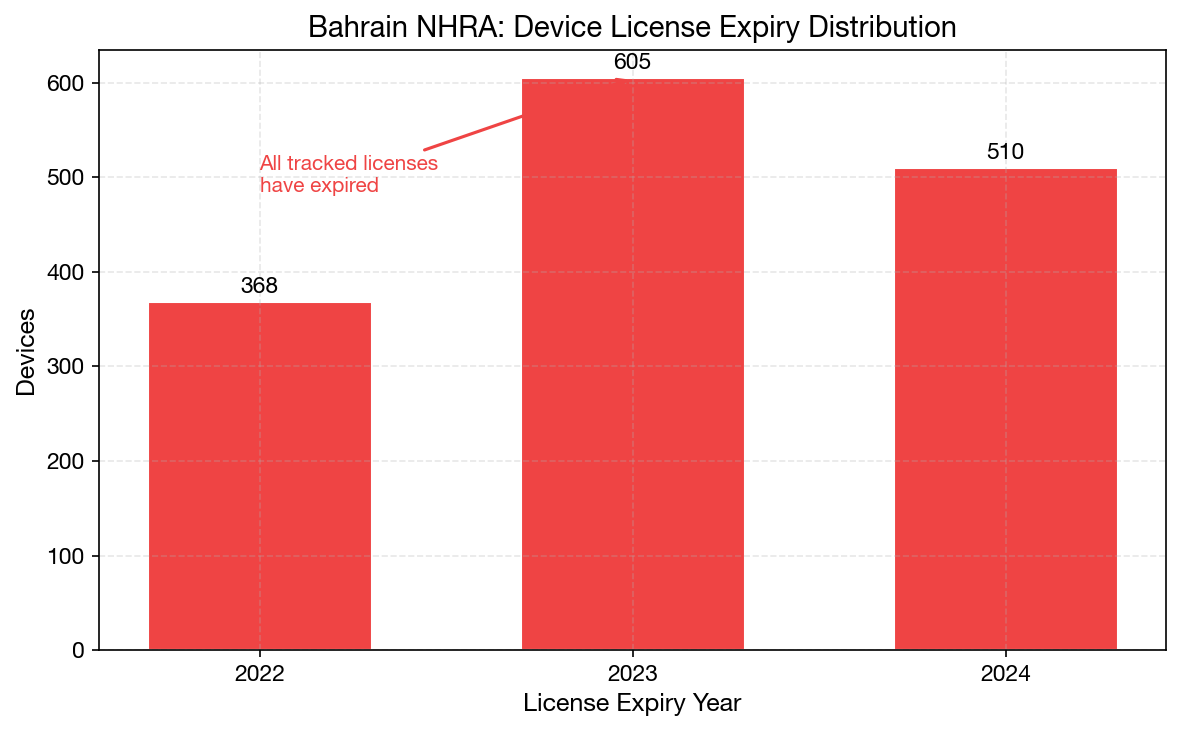

License Expiry Status

All tracked license expiry dates in the dataset fall between 2022 and 2024:

| Expiry Year | Devices |

|---|---|

| 2022 | 368 |

| 2023 | 605 |

| 2024 | 510 |

This confirms the dataset captures the pre-mandatory-registration landscape — devices that were listed before NHRA's 1 February 2026 mandatory deadline. These registrations will need renewal under the new mandatory framework, creating a one-time surge in regulatory activity as manufacturers and ARs bring their portfolios into compliance.

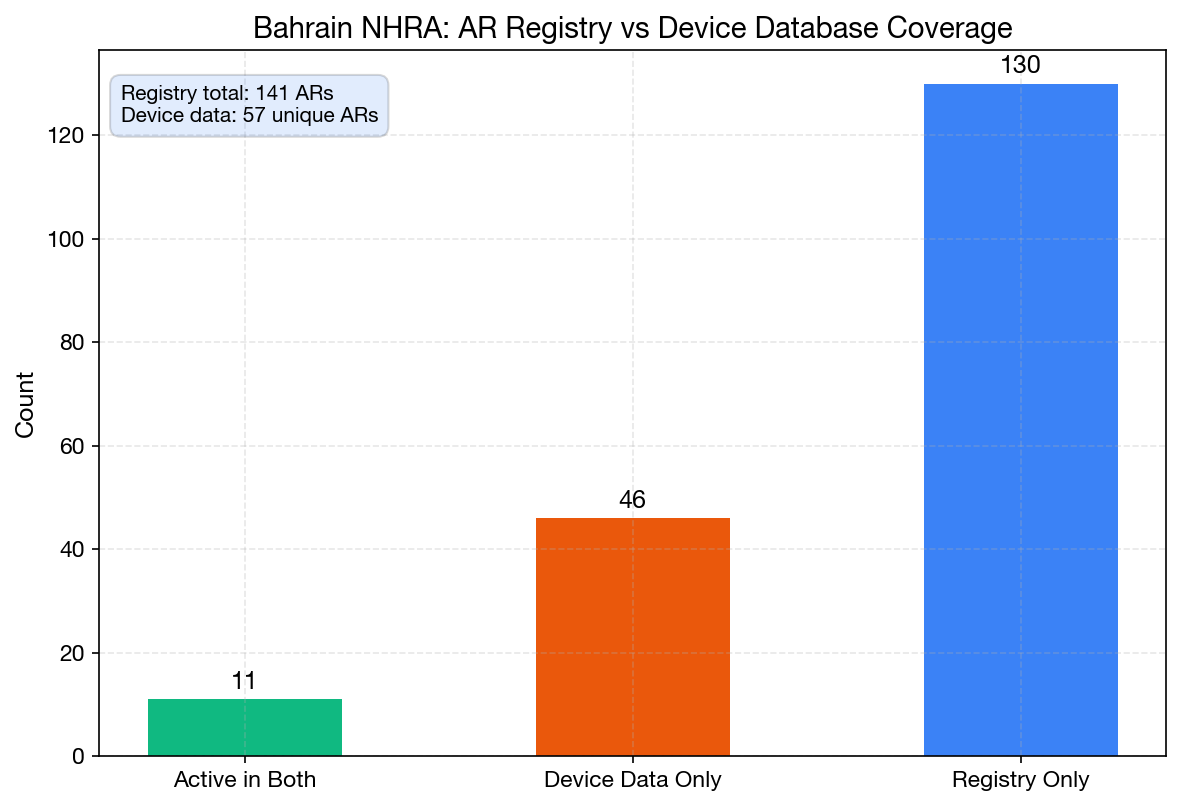

AR Registry vs Device Database

The AR registry lists 142 companies, but only 62 appear in the device database. This gap reflects several dynamics:

- Many registered ARs are newly licensed and have not yet accumulated device registrations under the mandatory regime

- Some ARs specialize in specific therapeutic areas (dentistry, ophthalmology, laboratory) and may hold registrations not captured in the device extract

- The device dataset predates mandatory registration, so ARs registered after the source PDF date would not appear

The 80+ ARs with no device listings in the historical data represent the available capacity in Bahrain's market — new entrants that may offer competitive terms to manufacturers looking for representation.

GCC Channel Strategy Implications

Bahrain's market structure illustrates a broader GCC pattern that affects market-entry decisions across the Gulf:

1. Each GCC State Requires Separate Registration

Unlike the EU's centralized CE marking, there is no single medical device registration covering all GCC states. Each country — Saudi Arabia (SFDA), UAE (MoHAP/EDE), Bahrain (NHRA), Qatar (MOPH), Kuwait (MoH), Oman (MoH) — requires its own national registration with a local AR. The Gulf Health Council's centralized procedure covers pharmaceuticals, not devices.

2. Small Market, High Fixed Costs

With only 1,491 registered devices (pre-mandatory), Bahrain's market is small. But the regulatory costs — AR appointment, documentation preparation, Ajheza system submissions, Arabic labeling, and annual renewals — are comparable to larger markets. This creates a high cost-per-device ratio that favors manufacturers with broad portfolios over those entering with a single product.

3. GCC Cross-Reference Recognition

NHRA accepts devices with existing approvals from reference regulators (US FDA, EU CE marking, Saudi SFDA) for streamlined registration. Manufacturers already registered in Saudi Arabia or the EU can leverage those approvals to accelerate Bahrain registration, but they still need a separate local AR.

4. UDI Traceability From July 2026

NHRA's UDI-based traceability system (enforcement from 1 July 2026) requires manufacturers to register device identifiers, upload pre-market data, and ensure labeling compliance. ARs will play a central role in managing this data, adding another layer of dependency on the chosen representative.

Practical Recommendations

| Consideration | Recommendation |

|---|---|

| AR selection | Prioritize ARs with established relationships with NHRA and experience in your device category |

| Portfolio strategy | Batch registrations to amortize fixed costs across multiple devices |

| GCC coordination | Consider ARs with presence across multiple GCC states (e.g., Cigalah operates in Saudi Arabia and Bahrain) |

| Switching planning | AR transfer is a minor variation; plan during the 1-year validity window to avoid renewal disruption |

| Post-mandatory surge | Expect processing delays in 2026-2027 as NHRA handles the registration backlog from newly mandatory devices |

Method Notes

- AR names were analyzed case-insensitively but displayed as-is from the database. Known variants (e.g., "General Medicals W.L.L" vs "general Medical") were noted but counted separately in the main analysis.

- Manufacturer names were extracted from the

legal_manufacturerfield (falling back tophysical_manufacturer). The source data contains OCR artifacts from PDF extraction that may affect name matching. - All 1,491 device rows trace to a single source PDF (

Registered_Devices_06_Aug_2023.pdf), confirming this is a point-in-time historical extract. - The AR registry (

nhra_authorized_representatives_20260605.csv) is a separate dataset with 142 entries containing company name, address, specialization, and license dates.

Data source: Bahrain NHRA registered-device database and AR registry; analysis by MedDeviceGuide, run date 2026-06-06.